What to Look for When Buying a Company

What to Look for When Buying a Company

Natalie Luneva

December 3, 2025

Buying a company follows a clear sequence: define what you want, screen quickly, verify everything, structure the deal, and plan the transition before close. Set strict criteria, cash flow, margins, customer mix, industry fit, so you can eliminate weak opportunities fast. When a business qualifies, request high-level financials, sign an NDA, and move into structured diligence: match tax returns to financials, test working capital needs, check customer concentration, evaluate processes, and verify claims with documents and third-party references.

Legal diligence runs in parallel: entity documents, licenses, liens, lawsuits, contracts, and compliance. With validated numbers, build a 12–24 month cash-flow model, triangulate valuation, and negotiate a deal structure, asset purchase, stock purchase, seller financing, earnouts, and escrows that protect you from hidden risks. Before closing, prepare a day-one plan covering payroll, banking, insurance, access, vendor communication, and the owner handover.

This guide walks you through how to buy a company and what to look for at each step so you can buy the right company with confidence and control.

Start with a clear roadmap that guides each step from first contact through final purchase. Expect to sign an NDA before receiving sensitive information. Set up an LLC or corporation so personal liability stays separate. Given that 70–75% of acquisitions fail to meet their objectives, tighten your process early.

Map a screening process: outreach, NDA, data-room review, management calls, site visits, and reference checks. Formalize diligence across financials, legal, operations, commercial, HR, compliance, and technology to keep efforts focused.

Recruit specialists early. Hire an acquisition attorney for agreements and an accountant for financial validation. Prepare monthly projections for 12–24 months to estimate working capital and cash needs tied to seasonality in the market.

Begin with a short market scan that ties local signals to national direction and forecasts. Verify recent growth against long-term trends and check customer stability. This helps you separate real strength from temporary spikes.

Map direct rivals and substitute businesses, then note switching costs and pricing power. Assess barriers that protect margin and whether new entrants can erode share. Confirm vendor dependencies and logistics limits that raise operational risks.

Speak with suppliers, nearby firms, and the chamber of commerce to corroborate demand signals. Analyze regulatory shifts, input costs, technology changes, and consumer behavior that affect sales patterns.

Connect these findings back into your financial model so valuation, profit forecasts, and deal structure reflect market realities rather than optimism. Document all insights as part of diligence.

.webp)

Confirm why the seller chose this sale and test that account against records, timelines, and third-party references. Motives like retirement, burnout, health, or partner disputes often carry different operational or transition implications. Verify statements with performance data and independent refs.

Ask the seller directly about timing and plans. Cross-check with financial trends and communications. If the owner plans to stay part-time, plan a formal handover to protect key relationships.

Reconcile customer-level revenue and contact top accounts with consent. Map supplier single points of failure and substitution options. Quantify how a lost customer or delayed shipment affects cash flow.

Search online reviews, regulatory records, and cyber incident histories. Negative publicity or compliance actions can signal hidden issues and reduce valuation.

Anchor price discussions in repeatable cash generation, not transient spikes. Normalize earnings and removing owner perks and one-time gains. That reveals true cash flow and helps test debt service capacity under realistic scenarios.

Normalize earnings and exclude nonrecurring items and owner-specific costs. Analyze free cash flow to confirm the business covers operations, debt service, and reinvestment without tapping reserves.

Review the balance sheet for machinery, inventory, and real estate. Validate intangible assets, trademarks, domains, and proprietary processes, and confirm legal ownership or transfers.

Benchmark using revenue or profit multiples from comparable private sales. Adjust multiples for size, growth, margin quality, and concentration factors that affect value.

Start your financial review and scan monthly trends for sudden shifts in revenue, margins, or cash timing. Focus on recent months first, then expand the lens to several years. This helps you spot drifts that affect valuation and capital needs.

Reviewing Income Statements, Balance Sheets, And Tax Returns

Reconcile income statements, balance sheets, general ledgers, and tax returns across multiple years to verify consistency. Have an accountant validate add-backs and tax filings. Cross-check bank statements against reported sales and expense lines.

Working Capital Needs And Seasonality

Break out sales by product, channel, and customer cohort to identify seasonal peaks and troughs. Assess AR aging, inventory turns, and AP terms to gauge working capital. Build a 12–24 month projection that links historical patterns to expected market conditions.

Compile a clear list of information gaps and require documentation for any anomalies. That list becomes your working due diligence checklist and shapes final offers, escrows, and post-close capital planning.

Before any offer, verify state filings and governing documents that prove the seller can transfer control. Start with charter documents, bylaws, resolutions, and operating agreements. Confirm registration is current and the entity is in good standing with state authorities.

Run searches for litigation, liens, and judgments. Identify open suits or encumbrances that could create ongoing liabilities after closing. Have your counsel summarize risk and remedies.

Review insurance policies, limits, exclusions, and claims history. Verify coverage actually transfers or that the seller will cure gaps. Note any pending claims that could breach representations.

Confirm all licenses and permits at federal, state, and local levels are current. Check renewals, specialty approvals, and any regulatory conditions that carry fines or suspensions.

Assess zoning compliance and environmental risk tied to property. Identify potential cleanup liabilities or use restrictions that could interrupt operations.

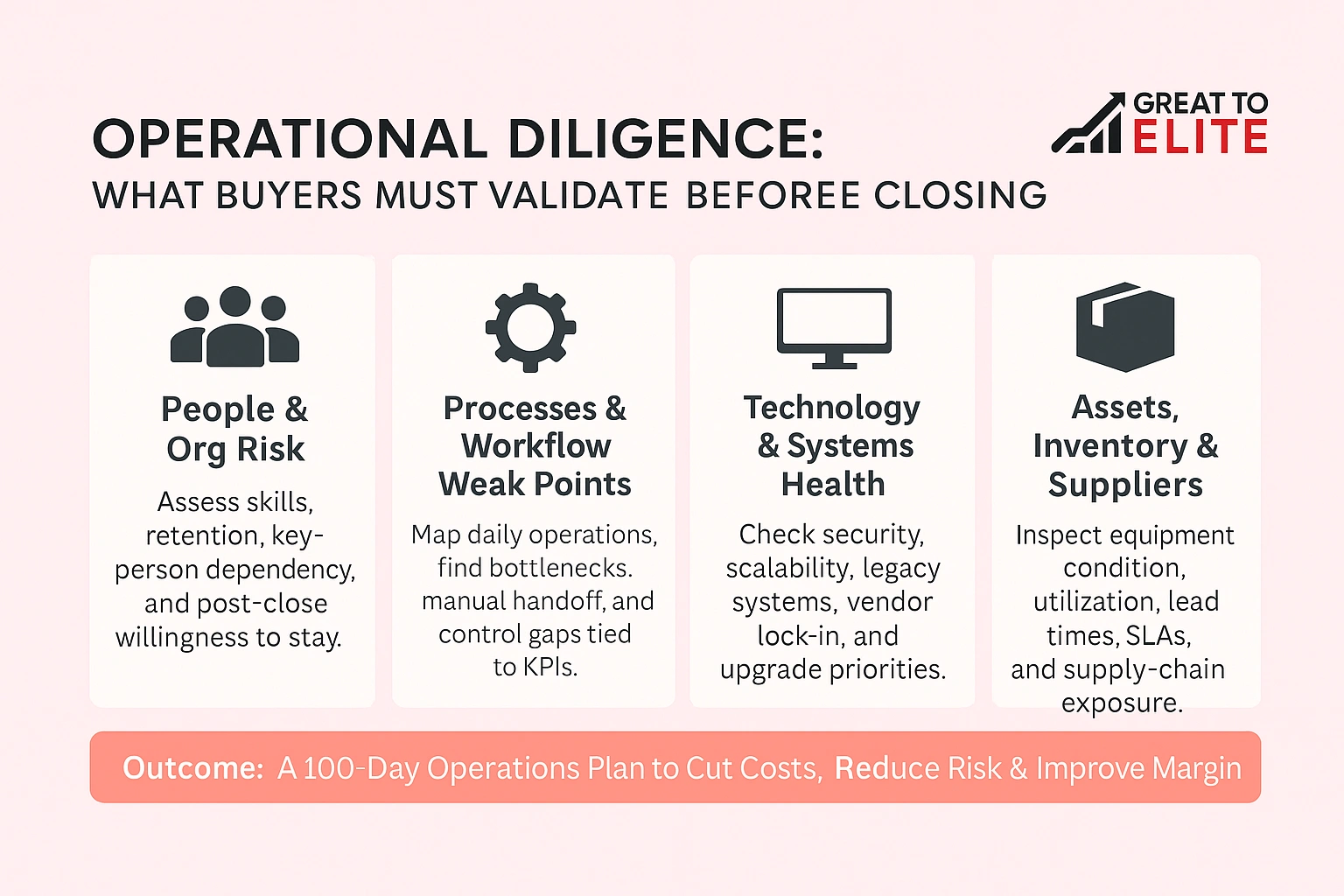

Map daily shop-floor work and digital workflows so you see where value is created and lost. Interview employees to assess skill levels, retention risk, and willingness to stay after close. Build an org chart that flags key-person exposure and retention levers.

Evaluate core processes end-to-end. Identify manual handoffs, bottlenecks, and control gaps that raise costs and slow throughput. Tie each process back to an operational KPI that links with financial outcomes.

Assess the technology stack for security, scalability, and vendor lock-in. Note legacy systems that increase risks and plan upgrades that lower costs and speed reporting.

Deliverable: a 100-day operations plan that quantifies cost savings from process fixes and technology modernization, prioritizes CapEx, and aligns KPIs with margin and cash.

Inspect two years of buyer records and contracts to measure repeat purchases, churn, and true revenue consistency. Reconcile lists in the CRM with accounting and AR aging so totals match recorded receipts.

Reconcile customer lists with ledger entries to confirm revenue by account and repeat behavior. Identify top buyers and quantify concentration risk.

Search reviews, social posts, and local media for negative signals that could hit future sales or lender confidence. Map NPS, complaints, and testimonial patterns to retention and wallet share.

Begin with an itemized inventory that ties listed assets back to the balance sheet. Request values, serial numbers, and proof of ownership for high-value items. Physically verify equipment and inventory during site visits.

Confirm clear title on any real property and search for liens or UCC filings. Verify zoning compliance and note any environmental exposure so the transaction price reflects remediation risk.

Inspect inventory quality and obsolescence controls. Review maintenance logs for equipment and estimate replacement timing. Reconcile counts with reported working capital and adjust valuations where shrinkage or wear exists.

Verify registrations are current and that assignments will transfer at closing. Review software licenses, source code ownership, and vendor contracts to avoid post-close access issues. Ensure IP rights materially support business value.

Select a framework that balances tax outcomes, seller needs, and liability exposure. Early structure choices shape financing, taxes, and operational risk after close. Define whether an asset or stock purchase fits your risk tolerance and tax plan before drafting offers.

Asset purchases limit unknown liabilities and let you pick specific items and contracts. Stock purchases may simplify transition but can carry legacy obligations and different tax results.

Use the LOI to lock exclusivity and outline price, structure, timelines, non-compete, access rights, and the diligence process. Clear milestones keep both parties accountable and reduce wasted legal spend.

Bridge valuation gaps with seller notes, earnouts, and working capital adjustments. These tools align incentives and protect against value leakage between signing and close.

Negotiate reps, caps, baskets, survival periods, and escrow mechanics that provide real recourse. Confirm critical contracts permit assignment or include timely consent obligations.

Prioritize a step-by-step handoff that captures systems, contacts, and daily routines from the outgoing owner. Plan a day-one checklist covering payroll, banking, insurance, and secure access so operations continue without interruption. Document critical systems and credentials and test logins before close.

Schedule structured sessions with the owner that include documented SOPs, key contacts, and role-by-role walkthroughs. Record training, capture vendor and customer scripts, and create quick reference guides for common issues.

Execute non-compete and non-solicit agreements that protect relationships and goodwill during the transition. Tie handover milestones to any seller earnouts or notes so incentives align with successful transfer of knowledge.

Announce the deal early and clearly. Tell employees about roles, support, and near-term priorities to retain talent. Share a concise message with customers and vendors that reassures continuity, service levels, and new points of contact.

Great to Elite supports business buyers by turning an acquisition into a smooth, high-confidence transition with clear systems, operational structure, and hands-on guidance. Their process starts with a diagnostic Scorecard that uncovers weaknesses across money, operations, growth, people, and owner freedom. From there, they create a customized roadmap and embed the systems, playbooks, and coaching needed to stabilize the business, improve margins, and make operations predictable from day one.

When a buyer works with Great to Elite, they get:

The result is a newly acquired business that runs smoother, generates healthier margins, and gives buyers confidence that the deal will perform as expected.

Ready to move forward? Book a call with Great to Elite and get a tailored plan that aligns market insights, contracts, and operations with your acquisition thesis. We help you capture value quickly and reduce execution risk so the deal delivers as expected.

A disciplined acquisition ends with clear priorities that protect value and speed operational gains. Anchor your choices in market validation, customer signals, and normalized cash flow so valuation and structure match reality.

Run thorough due diligence and document issues so you can reflect risks in price, escrows, and seller reps. Speak with sellers, vendors, and employees, then validate claims with independent analysis.

Map liabilities, capital needs, and compliance obligations ahead of close. Invest early in operations, SOPs, and leadership rhythms so the business sustains customers and cash during transition.

When you are ready to move from evaluation to execution, partner with experienced operators who help integrate, grow, and create durable value after acquisition.