Enterprise Value Calculator

What Is Enterprise Value?

Think of enterprise value as the theoretical takeover price – what it would actually cost to acquire the entire business. This metric is particularly valuable when comparing companies with different capital structures or debt levels.

Why Enterprise Value Matters

Enterprise Value Formula Explained

Let's break down each component:

Market Capitalization

Market capitalization represents the total value of a company's outstanding common shares. Calculate it by multiplying the current share price by the number of shares outstanding:

Market Cap = Share Price × Shares Outstanding

For public companies, this information is readily available. For private companies, you'll need to estimate equity value through comparable company analysis or discounted cash flow methods.

Total Debt

Total debt includes all interest-bearing liabilities, both short-term and long-term. This encompasses:

- Short-term borrowings

- Current portion of long-term debt

- Long-term debt

- Capital lease obligations

These figures can be found on the company's balance sheet under current and non-current liabilities.

Cash and Cash Equivalents

Cash and cash equivalents include highly liquid assets that can be readily converted to cash, such as:

- Cash on hand

- Bank deposits

- Short-term investments (maturity under 90 days)

- Marketable securities

This amount is subtracted because an acquirer would effectively receive this cash upon acquisition, reducing the net purchase price.

Preferred Stock and Minority Interest

These additional components represent claims on the company by parties other than common equity holders:

- Preferred Stock: Shares with priority over common stock for dividends and assets

- Minority Interest: The portion of subsidiaries not owned by the parent company

Enterprise Value Calculator

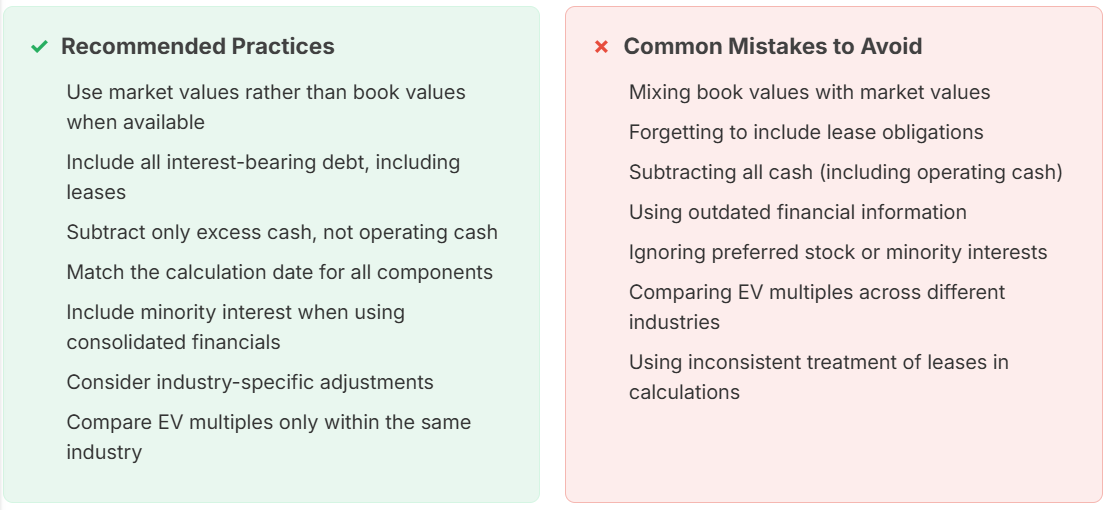

Best Practices for Enterprise Value Calculation

Practical Applications of Enterprise Value

Enterprise value multiples vary significantly across industries due to differences in growth rates, capital intensity, and risk profiles. Here are typical EV/EBITDA ranges by sector:

Enterprise Value Multiples by Industry

Enterprise value multiples vary significantly across industries due to differences in growth rates, capital intensity, and risk profiles. Here are typical EV/EBITDA ranges by sector:

When using these benchmarks, remember that company-specific factors like competitive position, management quality, and growth trajectory can cause significant variations within the same industry.

Have Questions? We Have Got Answers