How to Buy a Company: The Complete Guide

How to Buy a Company: The Complete Guide

Natalie Luneva

November 27, 2025

Buying a company is one of the fastest ways to step into proven revenue, existing customers, and an operating model that already works. Instead of starting from zero, you acquire momentum. But getting a deal across the finish line takes more than interest; it takes a clear, structured process. The moment you decide to buy a business, your path begins with defining what you want, researching targets, and verifying that the numbers and operations truly support the price.

When you buy a company, you move through four core stages: preparation, sourcing, due diligence, and closing. Preparation clarifies your budget, preferred industries, financing options, and the size of business you can realistically acquire. Sourcing introduces you to on-market and off-market opportunities through brokers, listings, and industry networks.

Due diligence digs into financials, customer concentration, legal risks, and operational health so you know exactly what you’re buying. And closing combines negotiation, financing, contracts, and transition planning so the handoff is smooth and the business keeps running from day one.

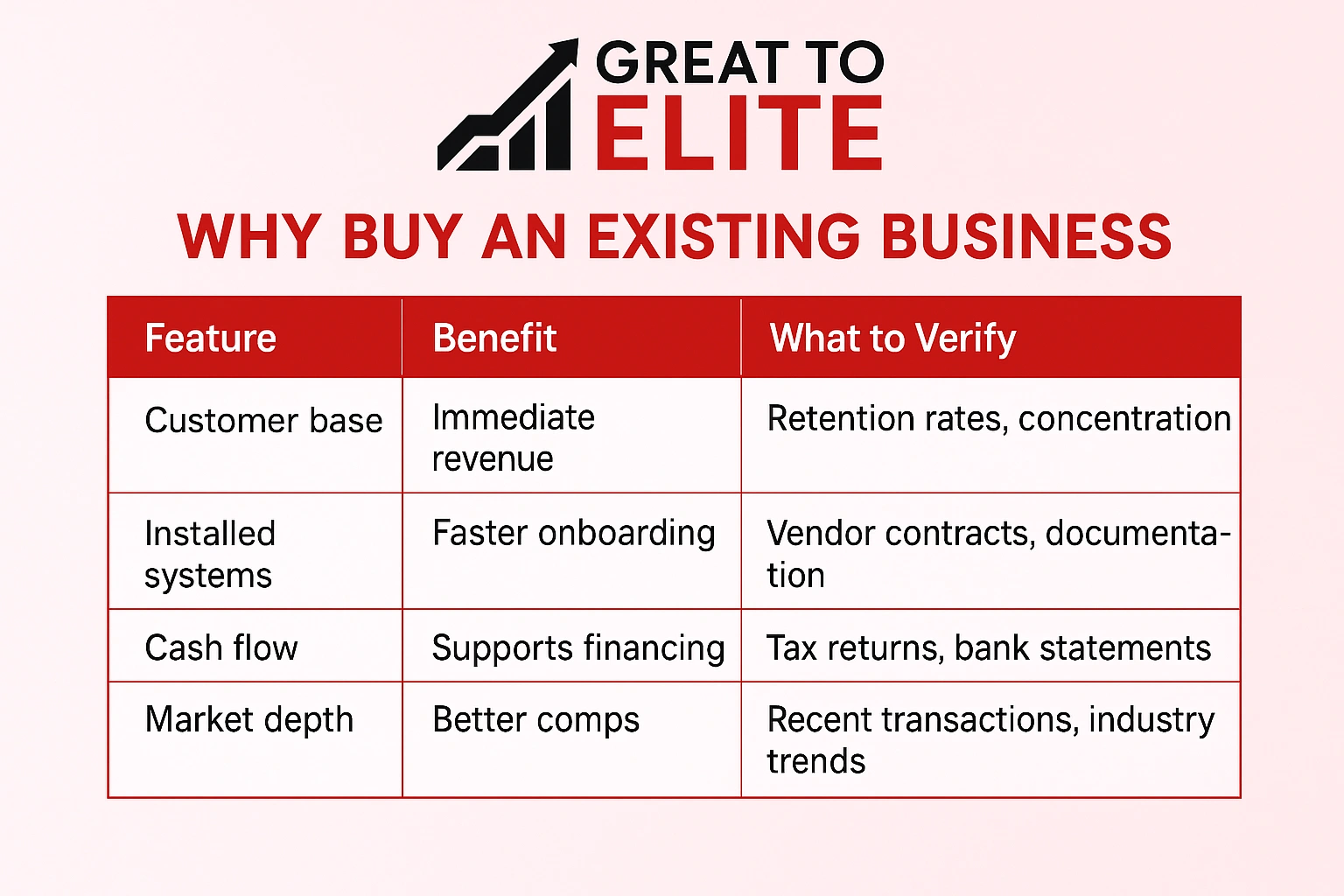

An active business brings momentum: customers, cash flow, and tested processes that speed results. You skip long setup phases and can focus on growth instead of building core systems from scratch.

When you step into an existing business, trained staff and vendor relationships cut onboarding time. That stability helps support debt service and early reinvestment, provided numbers are verified.

Check for owner dependence and revenue concentration. Some listings are for distressed operations, so trends and client mix matter before you advance a deal.

For the full year of 2024, global M&A volume reached approximately $3.4 trillion, with the U.S. accounting for around 50% of the activity. This depth means active buyers, lenders, and market data you can use for comps and price context.

Aligning your experience, available hours, and tolerance for risk narrows searches and lowers execution risk. Clarify what you can run well and what you cannot. That clarity saves time and prevents chasing deals that look good on paper but fail in practice.

List your core skills and the daily time you can commit. Some models need hands-on leadership; others run on documented systems.

Set risk bounds for finance and operations. Knowing your appetite helps you choose size thresholds that match debt capacity and resources.

Narrow by industry familiarity to shorten the learning curve. Pick revenue and headcount ranges that fit your plan for growth.

Start your search with channels that actually produce vetted opportunities in the U.S. market. Cast a wide net across online marketplaces, reputable brokers, and your local network. Each source brings different lead quality and verification standards.

Focus on listings that include clear financial statements and a believable seller narrative. That saves time and reduces wasted effort.

Market listings can show volume, but screen for documentation before deeper review.

Brokers often pre-vet sellers and can surface deals that match your criteria.

Your network and word-of-mouth find quieter opportunities and spares public competition.

A clear valuation framework helps you turn financials into a defensible offer. Match the method to the business profile and the data you can verify.

For many small firms, earnings multiples offer a fast baseline. Small, steady operations often trade at roughly 2x–4x normalized earnings. Confirm this against multi-year records and a quality-of-earnings line-by-line review.

Use discounted cash flow when margins or growth will change over the next years. DCF captures planned initiatives, but it requires realistic revenue and capex assumptions.

Apply an asset-based approach when tangible assets drive most of the value. Adjust for fair market value and remaining useful life.

Market comparables help when recent, local sales exist. Remember that sparse or uneven sales data can mislead price expectations.

Qualitative factors, owner dependence, staff depth, reputation, and scalability, move multiples up or down. Model conservative scenarios for volume and margins so you don’t overpay.

Financing choices shape deal timing, monthly cash flow, and your ability to preserve working capital after close. Pick paths that match your risk appetite and the business profile while meeting lender documentation needs.

SBA-backed loans can cover up to about 90% and often run up to 10 years. Expect competitive rates, low down payment needs, and an approvals process that can take several weeks.

Typical lender asks include strong personal credit, multi-year financials, and a clear business plan. Prepare tax returns, bank statements, and forecasts before applying.

Seller notes let you spread part of the price over time and bridge valuation gaps. They reduce immediate cash needs and align incentives but may include covenants or standby clauses if paired with SBA debt.

Traditional lenders require more down payment and scrutinize collateral, industry experience, and cash coverage. Investor capital brings governance and growth support but creates dilution and reporting obligations.

Personal funds or retirement rollovers offer direct control but carry tax and risk implications. Many buyers use blended structures, SBA plus seller note and a small equity check, to optimize price and preserve reserves.

Due diligence separates confident offers from costly mistakes when evaluating an operating business. Plan a focused review that treats each area as a gate: fail any gate, and you either walk or renegotiate.

Request three years of P&L, balance sheets, cash flow statements, and tax returns. Reconcile reported revenue with bank activity and payroll. Analyze seasonality and stress-test cash flow for debt coverage.

Inspect contracts, leases, and permits for transferability and change-of-control clauses. Search for pending litigation and confirm insurance limits. Note any regulatory gaps that could create future liability.

Review the org chart, compensation, and retention risk for key staff. Walk core processes from sales intake through billing to verify documented procedures match practice. Audit vendor terms, equipment age, and inventory condition.

Diligence often ends deals; accept that outcome as protection. When you catch a material problem, you’ve saved money, time, and future headaches.

Start negotiations and define what changes hands, the payment mix, and which contingencies protect your capital. A clear letter of intent lets both sides agree on the framework before deep diligence begins.

In the LOI, state the proposed price, which assets and contracts are included, payment terms, and an exclusivity window. Include contingencies for financing, satisfactory diligence, and third-party consents so you can walk if fundamentals shift.

Spell out cash at close, seller note mechanics, and any earn-out triggers. Use holdbacks or escrow for known risks and link earn-outs to measurable business metrics.

Negotiate specific owner support: training hours, customer introductions, and vendor handoffs. Define durations and deliverables so both sides measure performance objectively.

Draft the letter so it dovetails with the definitive agreement. That reduces re-trading and keeps the deal aligned with financing and diligence realities.

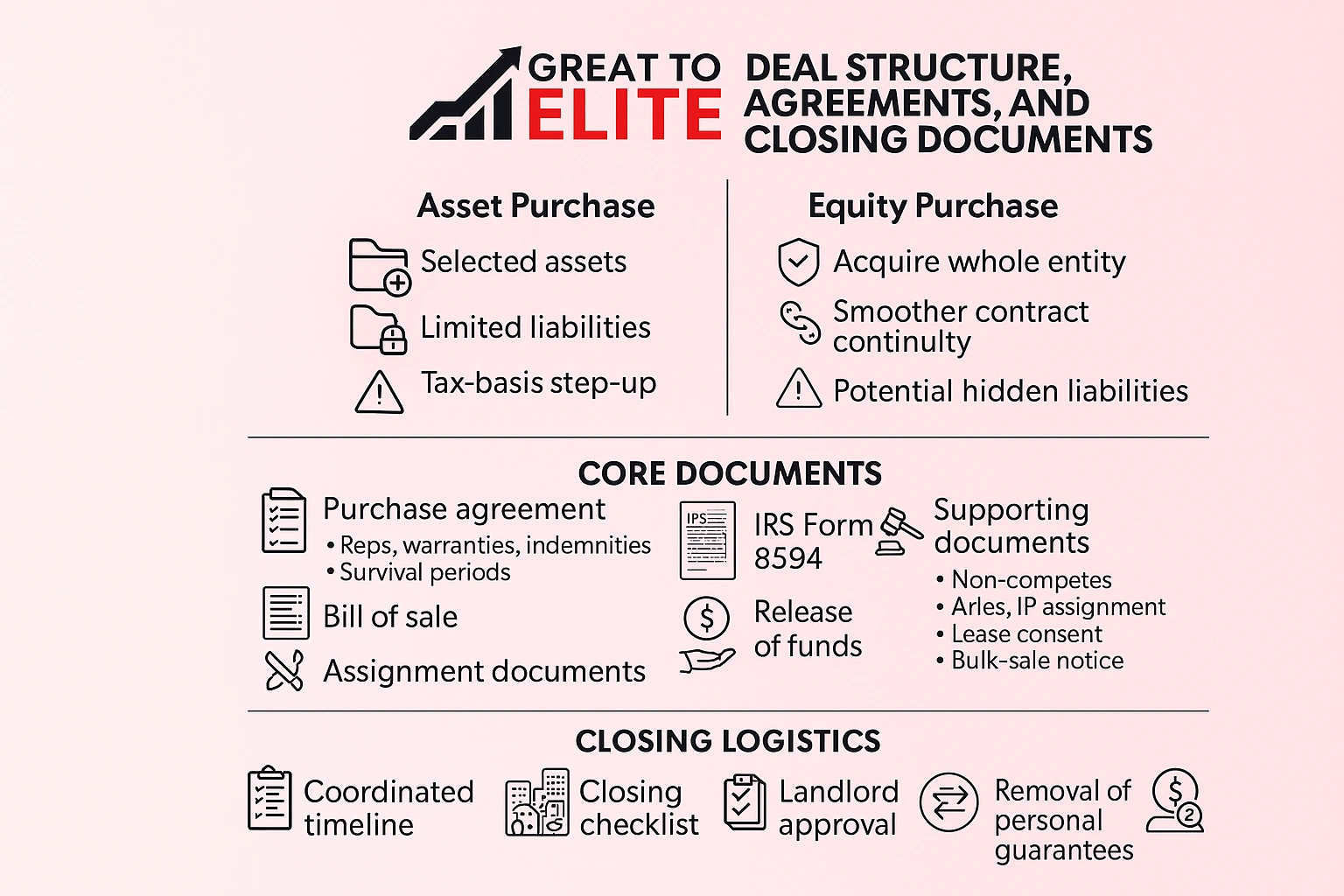

Select the transaction format that matches your risk appetite, lender requirements, and tax plan. That decision guides consents, liability exposure, and which documents you must deliver at closing.

In an asset purchase you pick specific assets and assumed liabilities. This often limits legacy liability and can step up asset basis for tax benefit.

In an equity purchase you acquire the entity outright. That eases continuity for licenses and contracts but may include hidden liabilities.

The purchase agreement should allocate risk through clear representations, warranties, indemnities, and survival periods.

Coordinate lender schedules, required certifications, and release of funds with the closing checklist. Confirm landlord approvals, review personal guarantees, and budget legal and filing costs plus a modest working capital cushion so the business runs on day one.

Start the post-close phase with clear milestones that protect revenue and keep the team focused. Use a short, structured plan that balances immediate stability with gradual change.

Agree on seller availability for 30–90 days and set weekly agendas for knowledge transfer. Record sessions and capture tribal knowledge in written guides.

Tell the team what will change, what stays the same, and who will make decisions. Clear messages reduce uncertainty and lower retention risk.

Prioritize vendor and key customer introductions in the first week to preserve relationships and prevent service gaps.

Tighten billing, accelerate collections, and pause nonessential spend to protect cash and cash flow. These actions give you breathing room while you learn operations.

Run a 30-60-90 plan that sequences process fixes. Aim for early wins that preserve the revenue line before you alter major systems.

Risk creeps in quietly; catch it early with clear controls and simple protections. Deals often fail during due diligence when undisclosed debt, bad leases, or heavy owner dependence appear. Plan practical steps that reduce exposure and preserve value.

Map owner tasks and client relationships. Document who runs critical work and build redundancy before closing. That lowers retention risk and keeps operations steady.

Quantify customer concentration and set acceptable thresholds. If top clients account for most revenue, negotiate protections or staged payments tied to retention over the first years.

Scrub tax, payroll, and litigation records and tie protections to specific agreements. Use tighter representations and survival periods for high-risk items.

Service acquisitions need hands-on guidance; Great to Elite gives practical steps and templates you can use now.

You get focused support that fits people-driven models. The approach centers on preserving revenue and retaining staff while closing deals.

If you want a proven way to evaluate, negotiate, and integrate your next purchase, book a call with Great to Elite and get started with a clear plan and the right resources for your team.

.webp)

Use this summary as a checklist for clear decisions during any purchase of an existing business. Keep valuation realistic, confirm records, and plan integration so the purchase matches projected value and risk.

Frame your offer with a clear letter intent and defined terms that protect cash and set the path for the definitive agreement. Treat the transaction as layered: valuation, financing, documentation, and transition each matter.

Pick financing and capital mixes that preserve runway and buy time for early wins. Protect sales, retain key staff, and track leading indicators so value unfolds over the next years.

If you want expert help evaluating a target, shaping the agreement, and running the first 90 days, reach out to Great to Elite and start your process with confidence.