Small Business Succession Planning: A Complete Guide

Small Business Succession Planning: A Complete Guide

Natalie Luneva

December 25, 2025

Small business succession planning is the process of deciding in advance who will own your company, who will run it day to day, and how decisions are made when you step away due to retirement, disability, death, or a temporary absence. It is a separate, operational plan that works alongside estate documents but goes further and defines leadership authority, ownership transfer rules, and timing so the business continues without disruption.

For most small business owners, the company is their largest asset and the primary source of income for employees and families who depend on it. Without a clear succession plan, even a short absence can stall operations, freeze bank accounts, unsettle staff, and push clients toward competitors, yet 61% of family businesses in North America do not have a written, formal succession plan in place. Estate plans determine who inherits equity; succession plans determine who can sign contracts, approve spending, manage teams, and keep revenue flowing.

A practical roadmap lays out leadership, decision rights, and documents needed to keep your company steady.

Name who will take over leadership and specify day-to-day duties. Define which management decisions are pre-authorized during a temporary absence. That prevents confusion and keeps operations moving.

Make ownership transfer rules explicit. State whether remaining owners can or must buy an exiting owner’s interest and reference an operating or buy-sell agreement to make that enforceable.

Keep these plans and documents aligned and in one accessible place so your company can act fast under pressure.

Acting now preserves value for your heirs and keeps operations steady when the unexpected happens.

Assess immediate risks: death, disability, or a temporary absence. Define triggers so your plan activates automatically and work continues without guesswork.

When a trigger occurs, pre-set steps reduce confusion. Name an interim leader, set spending limits, and secure client communications to limit revenue loss.

Ownership transfer is not the same as who runs day-to-day work. Your plan should separate equity moves from operational roles so qualified leaders keep the company running.

Many owners hold most of their net worth in the company. Without a clear plan, heirs and stakeholders can face steep losses, delays, or forced sales at a discount.

About one-third of firms have a plan and nearly 70% fail to sell at retirement. Early work reduces buyer discounts, lowers tax surprises, and calms family disputes.

Fix a firm timeline that turns an abstract idea into actionable milestones. Set a clear exit goal three to five years out so you can sequence valuation work, grooming, and financial cleanup.

Work backward from your target date. Add checkpoints for valuation, debt cleanup, and buyer outreach.

Create a skills-based profile for candidates, family, partner, employee, or third party, and rate them objectively on leadership, financial acumen, and client relationships.

Clean the balance sheet, produce a reliable P&L, and consider an independent CPA review to boost buyer confidence.

Capture day-to-day processes, roles, and training guides so a new manager can follow a proven process from day one.

Match funding methods, insurance, loans, or seller financing, with tax advice to avoid surprises at close.

Tell key team members early to preserve morale, then inform the wider staff after closing or at a controlled point to protect retention.

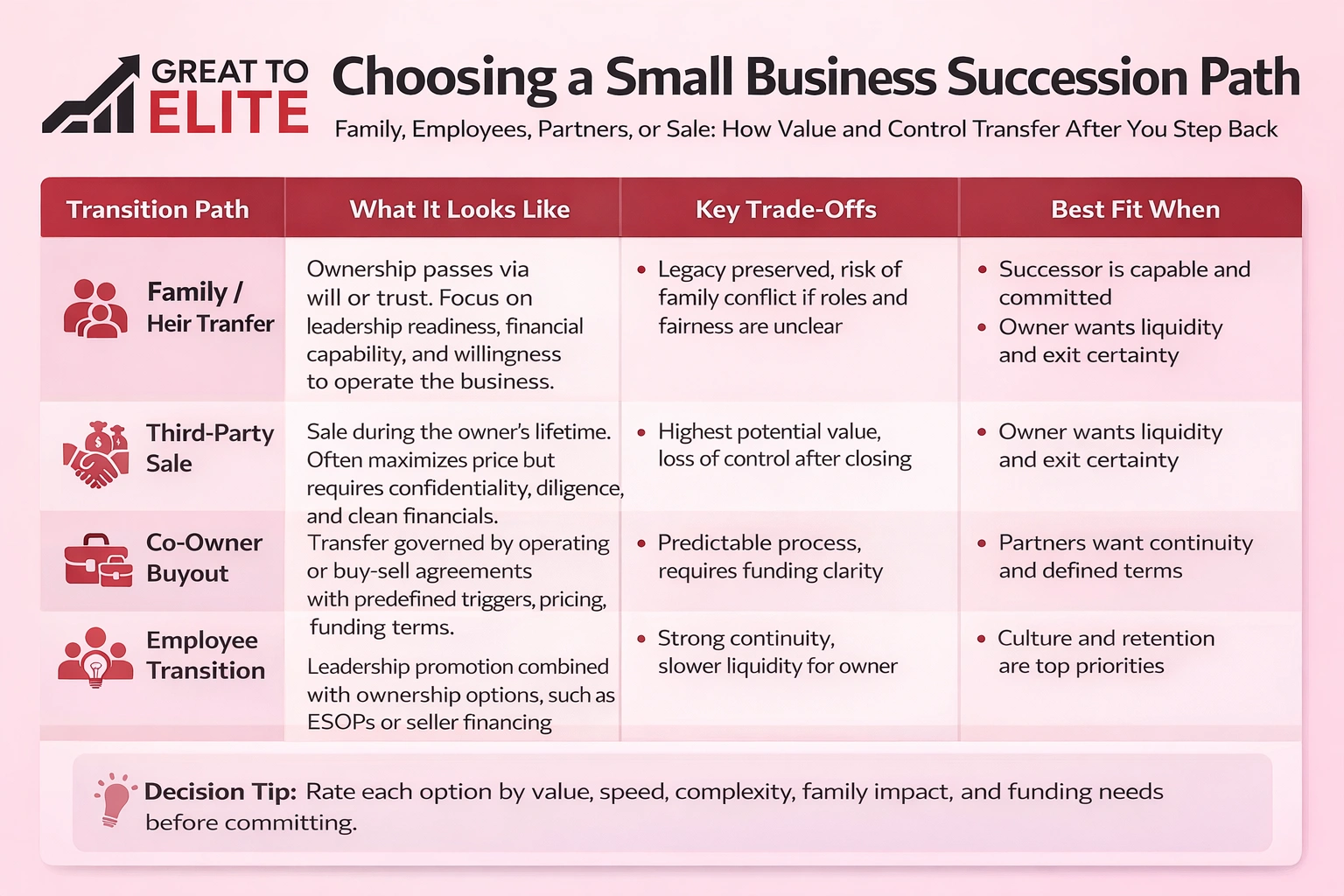

Choosing the right exit route shapes how value, control, and continuity travel after you step back. Compare the main types to match your goals for timing, cash needs, and culture.

Passing ownership via will or trust keeps things in the family and can preserve legacy. Evaluate readiness: leadership skills, financial ability, and willingness to run the company.

Plan fair treatment for relatives who do not work in the company to avoid conflict and claims that erode value.

Selling during your life typically maximizes price but adds confidentiality and due-diligence work. You can negotiate earnouts, warranties, and timing to protect value.

Third-party deals often move faster if financials are clean and key clients are secure.

Predefined operating or buy-sell terms remove guesswork. Use triggers, valuation formulas, and funding rules so owners know how a transfer will be priced and paid.

Funding clarity, insurance, loans, or staged payments, reduces interruption and preserves relationships among owners.

Employee transfers combine leadership promotion with broader ownership options like ESOPs or seller financing. This protects culture and continuity.

Design leadership placement, training, and retention incentives so clients and staff see steady management from day one.

Pinning down both price and payment sources makes business ownership succession moves practical and predictable.

Pick the method that matches your company’s size, growth outlook, and data quality. Common approaches are:

Buyers reward predictable profit, a clean balance sheet, and a diversified customer base.

Work to remove one-time expenses, tighten collections, and document recurring revenue. That raises perceived value and speeds selling business negotiations.

Common funding tools include life insurance, bank loans, internal reserves, or seller financing. Match the mix to cash needs and tax goals.

Decide if transfers use a fixed price or a formula tied to fair market value. Put update rules into the succession plan so owners avoid disputes later.

Tax-aware timing matters. Model tax outcomes, choose entity structure, and time payouts to keep more value in your pocket. That makes the transition more attractive to a successor and to lenders.

Gather the legal and operational files now so transfers run smoothly when a trigger occurs.

Compile core legal agreements that make ownership and price mechanics enforceable. Include wills and trusts for ownership interests, an operating agreement for decision authority, and a buy-sell agreement that states valuation methods and funding rules.

These documents define who owns what, when a transfer happens, and how payments are made. Make sure each paper names the owner, pricing formula, funding source, and trigger events.

Operational playbooks let a new leader keep operations steady from day one. Create SOPs, org charts, an employee handbook, and training guides that spell out daily tasks.

A smooth handoff hinges on defined roles, clear timing, and repeatable steps that everyone follows.

Orchestrate a formal leadership handover with documented duties, immediate priorities, and interim coverage. Appoint an interim leader who has spending limits and client contact rules.

Train that person on critical tasks and give access to advisors. Set governance and reporting rhythms so the new leader reports progress weekly at first.

Tell key staff early to protect morale and retention. Then announce widely at a controlled time, often after closing, to limit rumors and churn.

Use clear messages: who will lead, what changes to expect, and how roles will evolve. Offer retention incentives for essential roles.

Prepare for life after the deal. Talk with former owners, ask detailed questions of advisors, and create a post-exit plan that excites you.

Schedule milestones for leadership, systems, customers, and financial handoffs. A disciplined checklist reduces regret and keeps the future secure.

Great to Elite helps you turn a vague exit idea into a concrete roadmap with deadlines and owners. We work with business owners to make the plan practical and executable.

If you are a small business owner ready to start or refine your plan, book a call with Great to Elite. Get a tailored strategy, a clear timeline, and hands-on execution support from a trusted team.

A clear exit roadmap turns vague intentions into steps you can follow years before retirement.

Start now: name leaders, document daily roles, and validate financials so you protect value when you transfer ownership.

Align funding and tax choices early to avoid surprises and make selling business or a sale more attractive to buyers.

Use measurable milestones and review this plan each year over the next five years to stay on track.

Act with urgency. A structured process preserves customers, keeps employees steady, and helps owners reach their retirement goals with more value in hand.