You’re about to review a company and you need clear signals before you invest time, money, and reputation. Trust your gut if something feels off, even when surface numbers seem fine.

Missing or inaccurate financial records often top the list of concerns. Without clean statements, you can’t verify performance over the past few years or assess true stability.

Pay attention to odd sale stories, unresolved legal disputes, unclear IP ownership, overdue taxes, and dependence on a few clients. Operational warning signs, high turnover, aging equipment, or owner-dependent workflows, also quietly erode value.

Lenders who refuse financing, inflated valuation, or an industry in decline are market-level cues that merit caution. This guide from Great to Elite will help you move from signals to verified facts before you negotiate a purchase and decide whether to buy a company or walk away.

Key Takeaways

Spot both obvious and subtle warning signs early to avoid costly surprises.

Verify financial records thoroughly to confirm performance over recent years.

Probe seller stories and check for legal, tax, and IP liabilities.

Watch operational issues like turnover and aging equipment that hurt margins.

Use lender feedback and market trends as reality checks on valuation.

Why Spotting Red Flags Matters In A Business Acquisition

Smart buyers separate sales spin from verifiable facts before committing time or capital. You must review financial health, operational structure, and future potential, especially when buying a home service business like HVAC, plumbing, electrical, and roofing. With 70–75% of acquisitions failing to deliver their intended value, disciplined buyers treat this as a reminder that careful validation is not optional.

Thorough market analysis and compliance checks prevent inheriting costly problems. They also let you judge whether issues are fixable or structural in the industry and if the company fits your investment thesis.

You reduce execution risk when you validate statements and customer trends instead of relying on seller stories.

You avoid overpaying when you identify fixes that hurt cash flow, margins, or terminal value before drafting an LOI.

You gain negotiation leverage with documented deficiencies that justify price, terms, or structure changes.

You plan integration earlier to prevent handoff delays from undocumented processes or owner dependence.

Focus your research on verified statements, contracts, customers, and compliance. That approach speeds decisions, protects downside, and helps you present a clearer memo to lenders and partners.

Red Flags When Buying A Business: Quick-Scan Warning Signs

Early screening reveals which targets deserve deeper diligence and which need to be walked away from. Start with simple checks that take little time but uncover major risks.

Trust-Your-Gut Indicators You Shouldn’t Ignore

If the seller answers shift after basic questions, pause. Inconsistent stories on reason for sale, timing, or forecasts are troubling. Fast-close pressure paired with missing documents is an immediate red flag.

Seller pushes to close fast while withholding bank statements or contracts.

Lenders decline after their review, assume they found trouble you haven’t.

Poor online reviews showing repeated missed appointments or unresolved complaints.

When “Small” Issues Hint At Bigger Problems

Minor mismatches can stack into serious problems. Different customer counts, mismatched contract dates, or partial financials often point to larger gaps in records.

Incomplete access to aging reports or bank records, stop until full files are provided.

Rapid ownership churn or short hold periods, these can signal persistent operational trouble.

Request simple reference checks with customers and suppliers early to validate claims.

Ask for a basic data room checklist; reluctance to organize documents is itself a flag.

Action tip: Triage findings into immediate no-gos versus fixable items so you focus effort where it counts during due diligence.

Financial Red Flags That Undermine Value

Begin with the numbers: confirm that statements, tax returns, and bank records tell the same story. Inaccurate or incomplete financial information is the fastest path to a surprise after closing.

Inaccurate or Incomplete Financial Statements

Insist on full statements tied to bank records and tax filings for at least three years. Gaps, unexplained adjustments, or aggressive accounting methods can overstate earnings and valuation.

Excessive Debt and Weak Debt Service Coverage

Evaluate total debts, interest costs, and DSCR. If DSCR trends below 1.25, payments become fragile and operations can stall. Compare leverage to industry norms before you proceed.

Erratic or Declining Revenue and Margins

Analyze multi-year revenue by segment and season. Shrinking margins or year-over-year declines often indicate pricing pressure, lost customers, or cost issues that hit value.

Poor Cash Flow Management and Heavy Credit Use

Stress test cash flow with a 20% revenue dip to reveal reliance on credit lines for daily expenses. Recurring negative operating cash flow and heavy credit use are early signs of trouble.

Overvalued Assets, Unsellable Inventory, and Hidden Liabilities

Probe inventory composition and turnover; unsellable stock inflates working capital. Verify fixed-asset appraisals, claims of high-value equipment often fall short in practice. Scan for off-balance-sheet obligations, warranties, and contingent legal exposures.

Practical checks: reconcile AR aging to cash collections and flag sudden spikes.

Valuation checks: watch for capitalized operating costs or aggressive depreciation that boost reported profit.

The way work gets done reveals more about future performance than glossy forecasts. Focus on field operations, systems, and people to see if the company can scale after an acquisition.

High Employee Turnover and Leadership Instability

High churn often means poor culture and inconsistent service. Replacement costs vary by role, and weak organizational health cuts the chance of margin outperformance by about 50%.

Undocumented Processes and Overreliance on Key People

A lack of documented process creates training gaps and quality drift. If the owner holds tribal knowledge, continuity suffers post-close. Map workflows and test knowledge transfer readiness early.

Outdated Systems, Tools, and Technology

Legacy IT can eat 60–80% of IT budgets and slow digital moves. Old platforms cause errors, slow cycle time, and hidden upgrade costs that hit in year one.

Benchmark turnover and leadership churn.

Inventory tools, map critical workflows, and test field operations.

Model time and investment to fix gaps and link findings to financial performance.

Operational Issue

Impact

Quick Check

Remediation Time/Cost

High turnover

Service inconsistency, higher hiring cost

Compare tenure and exit reasons

3–9 months; moderate cost

Undocumented workflows

Training gaps, quality drift

Request SOPs and ride-alongs

1–6 months; low–medium cost

Legacy IT

Slow cycles, budget overruns

Audit systems and upgrade path

6–18 months; high cost

Customer, Supplier, And Concentration Risks

Concentration exposure can hollow out revenue fast, so quantify key relationships before you sign. List revenue by customer and supplier and flag any single account supplying more than 20% of sales.

Over-Reliance On One Or Two Clients

If one customer supplies over 20% of revenue, treat that as cautionary; over 50% is critical. Combined top-three clients above 50% raises systemic risk for the company and the planned acquisition.

Review contract lengths, renewal terms, and termination rights. Short runways or one-sided clauses increase fragility and deserve price adjustments or holdbacks.

Single-Supplier Dependencies And Vulnerable Contracts

Supplier concentration above 40% increases vulnerability to delays and cost shocks.

Verify lead times, backup options, and any exclusivity clauses. Negotiate supplier contingencies or transition assistance into the deal if disruption would be severe.

Weak Collections And Accounts Receivable Spikes

Large AR spikes or trending slow payments are early signs of cash stress. Reconcile aging buckets, dispute logs, and write-offs against revenue trends.

Consider earnouts tied to retention, escrow holdbacks, or seller support agreements to protect payments and key accounts during transition.

Quantify concentration by customer and supplier; convert thresholds into valuation adjustments.

Audit contracts for renewal timing, notice periods, and termination clauses.

Test relationship stability via customer satisfaction, tenure, and account-manager dependence.

Document all findings to align advisors and lenders on exposure and mitigation plans.

Risk

Threshold

Mitigation

Single customer reliance

>20% caution; >50% critical

Holdbacks, earnouts, retention covenants

Top-3 concentration

>50% combined

Price adjustment, diversification plan

Single supplier reliance

>40%

Alternate suppliers, inventory buffers

Legal, Compliance, And Tax Red Flags

Before you sign papers, verify every legal and tax item that could halt operations or drain cash. Start with a full catalog of litigation, regulatory actions, and potential exposure.

Pending Lawsuits and Regulatory Violations

List each claim, its stage, and a dollar estimate for loss and defense. Employment disputes and agency enforcement often signal management or culture problems.

Unresolved Tax Issues and Penalties

Reconcile tax filings to books and bank records. Late filings, audits, or unpaid balances can trigger liens or levies that survive an acquisition.

Zoning, Licensing, and Safety Gaps

Match permits and licenses to current operations and planned growth. Missing safety records or training logs suggest systemic compliance issues.

Confirm data privacy and security posture; breaches carry outsized fines and cleanup costs.

Interview counsel and compliance leads to assess program maturity, not just paperwork.

Align indemnities, escrows, and remediation timelines with known matters before close.

Risk Area

Immediate Check

Potential Impact

Mitigation

Litigation

Complete docket list and reserves

Large payouts, injunctions

Escrow, price reduction, indemnity

Tax

Reconcile returns to cash and books

Penalties, liens, enforced collections

Holdback, seller cure, escrow

Permits & Safety

Validate licenses and training records

Fines, shutdowns, slowed growth

Corrective plan, conditional close

Data & Privacy

Review breach history and controls

Regulatory fines, lost trust

Cyber insurance, remediation escrow

Intellectual Property And Data Risks You Must Validate

Confirming who truly owns core intellectual property stops surprises and protects future revenue. Lack of clear ownership lets competitors copy products or services and can erode market defensibility in your industry.

Focus first on chain of title for trademarks, patents, copyrights, and source code. Verify assignments from founders, contractors, and agencies so the company can enforce rights after an acquisition.

Scan license terms, territorial limits, and pending claims. Narrow patent scope or expired filings reduce pricing power and create due diligence issues you must quantify.

Verify trademark and patent filings and ownership links to the company.

Test vendor and contractor agreements for IP assignment and transferability.

Assess customer data handling, security controls, and legacy systems tied to core operations.

Address technical risk fast: map legacy IT, estimate upgrade cost, and align indemnities or escrow to known exposures. Weak practices in data privacy or outdated platforms can cause breaches, fines, and lost customer trust.

Risk

Quick Check

Primary Mitigation

Unclear IP ownership

Chain-of-title review

Assignment confirmations; escrows

Data/privacy gaps

Security controls and breach history

Remediation plan; cyber insurance

Legacy IT

Systems inventory and vendor contracts

Upgrade roadmap; cost reserves

Market And Industry Signals You Can’t Overlook

Scan local and national trends to confirm the company’s growth story matches reality.

Declining demand or a crowded service area can limit revenue and compress value fast. You must test forecasts against real signals, not just seller projections.

Declining markets, saturation, and lack of differentiation

Watch for shrinking demand, repeated price cuts, or low repeat rates. These signs often mean the market is moving to commodity pricing and profit slips.

Competitor movements that threaten share

New entrants, aggressive hires, or large tech investments by rivals can erode your target’s revenue. Track recent openings, marketing spend, and pricing changes in the service radius.

Benchmark multi-year demand vs GDP and peers to spot structural decline.

Map competitors, capacity, pricing, and win rates to test saturation.

Validate differentiation, service, warranties, tech, via mystery shops and customer calls.

Confirm forecasts with independent research and on-the-ground checks of local demand.

Stress-test pricing power under competitive pressure and macro shifts.

If lack of differentiation and negative signs stack up, avoid deals without a clear turnaround plan.

Signal

What to Check

Immediate Action

Time to Validate

Falling local demand

Revenue trends, permit data, job starts

Request region sales roll-up; call key customers

1–3 weeks

High competitor density

Competitor count, pricing, capacity

Map service radius and secret-shop

2–4 weeks

Weak differentiation

Unique services, warranties, response times

Test offers and ask customers about reasons for choice

1–2 weeks

Rival expansion

Hiring, new locations, tech spend

Monitor job boards and public filings

2–6 weeks

Seller-Related Red Flags And Deal Dynamics

Ask for proof that the seller’s rationale matches operating trends and customer data. Sellers often hide distress behind tidy explanations, so you must confirm motives with documents and interviews.

Suspicious Reason For Sale or History of Quick Flips

Multiple short ownership periods suggest recurring issues. Verify tenure, past sale notes, and customer churn to see if the pattern signals structural problems.

Pressure To Close Fast or Inconsistent Information

Rushed timelines reduce your leverage. Slow the process and insist on full access to records if you see pressure tactics or shifting answers.

Artificially Inflated Valuations and “No Problems” Claims

Get an independent valuation and challenge add-backs that lack recurrence. Treat claims of flawless operations skeptically and tie findings to price adjustments.

Owner-Dependent Companies With Understated Involvement

Map the owners’ daily tasks, sales, key accounts, estimating, and quantify transition needs. Plan retention pay, training, and overlap to protect customer continuity.

Verify the seller’s reason for sale against metrics like churn and payroll.

Slow the timeline when pressured; preserve negotiation leverage.

Obtain an independent valuation and challenge nonrecurring add-backs.

Document inconsistencies and tie them to price, structure, or walk-away points.

Risk

Quick Action

Negotiation Tool

Owner-dependent

Map duties; test replacements

Retention bonuses; transition services

Inflated valuation

Independent appraisal; verify add-backs

Price reduction; escrow holdbacks

Fast sale pressure

Pause timelines; request full docs

Conditional close; reps & warranties

Facilities, Equipment, And Contract Pitfalls

Site visits reveal contractual and asset issues that spreadsheets will miss. Inspecting premises early helps you spot lease cliffs, hidden cost hikes, and machines near end of life. These are common red flags that affect valuation, operations, and the timing of any sale.

Leases Near Renewal and Hidden Cost Hikes

Expiring leases can trigger major price increases or restrictive terms. Request renewal notices and landlord quotes. Review assignment rights and CAM charges so occupancy costs are modeled correctly.

Equipment Near End-Of-Life and Hard-To-Replace Parts

Run equipment while on site and examine maintenance logs. Older units raise downtime and parts lead times can be long. Confirm warranties and whether service contracts transfer to your entity.

Calendar lease expirations and request renewal quotes.

Inventory critical equipment by age, hours, and service history.

Test parts availability and lead times for legacy models.

Assess time and capex to modernize facilities and meet safety standards.

Tie asset condition to productivity and customer quality metrics.

Risk

Quick Check

Mitigation

Lease renewal spike

Review notice, CAM details

Negotiate price relief or term extensions

Obsolete equipment

Run and inspect units

Escrow for replacement; phased capex

Parts scarcity

Call vendors for lead times

Source alternates; stock critical items

Financing Barriers And What Lenders Are Telling You

Lenders often spot problems your checklist misses; treat their no as valuable intelligence. A decline to fund is rarely bureaucratic. It usually reflects concerns about cash flow, documentation, or long-term viability.

Declined Financing Due To Due Diligence Findings

If an underwriter rejects funding, ask for written feedback. Pinpoint whether the issue was unstable earnings, incomplete records, or unexpected debts.

Use that feedback to rebuild your model with conservative assumptions and to structure the deal with holdbacks or earnouts if you continue.

Poor Credit Scores and Payment History Problems

Weak credit and heavy use of revolving credit are clear negatives. Review vendor payment history, covenant projections, and the debt schedule.

Verify liens, UCC filings, and consistency between disclosures and public records. These checks prevent unpleasant surprises after close.

Treat a lender decline as a major signal, not a box to tick past.

Request precise underwriting reasons and correctable items.

Rebuild forecasts conservatively and add structural protections to the deal.

Decide to walk if fixes aren’t credible within a realistic timeline.

Issue Identified

Common Lender Concern

Immediate Buyer Action

Outcome If Unaddressed

Weak cash flow

Insufficient DSCR and volatile receipts

Stress-test model; tighten assumptions

Loan denial or harsh terms

Poor credit history

Late payments and defaults

Obtain credit reports; negotiate seller cures

Higher rates or refusal

Unresolved liens/UCCs

Hidden encumbrances on collateral

Reconcile filings and demand releases

Title problems; blocked financing

Documentation gaps

Missing tax returns or bank reconciliations

Require full file; pause deal timeline

Increased diligence, lost leverage

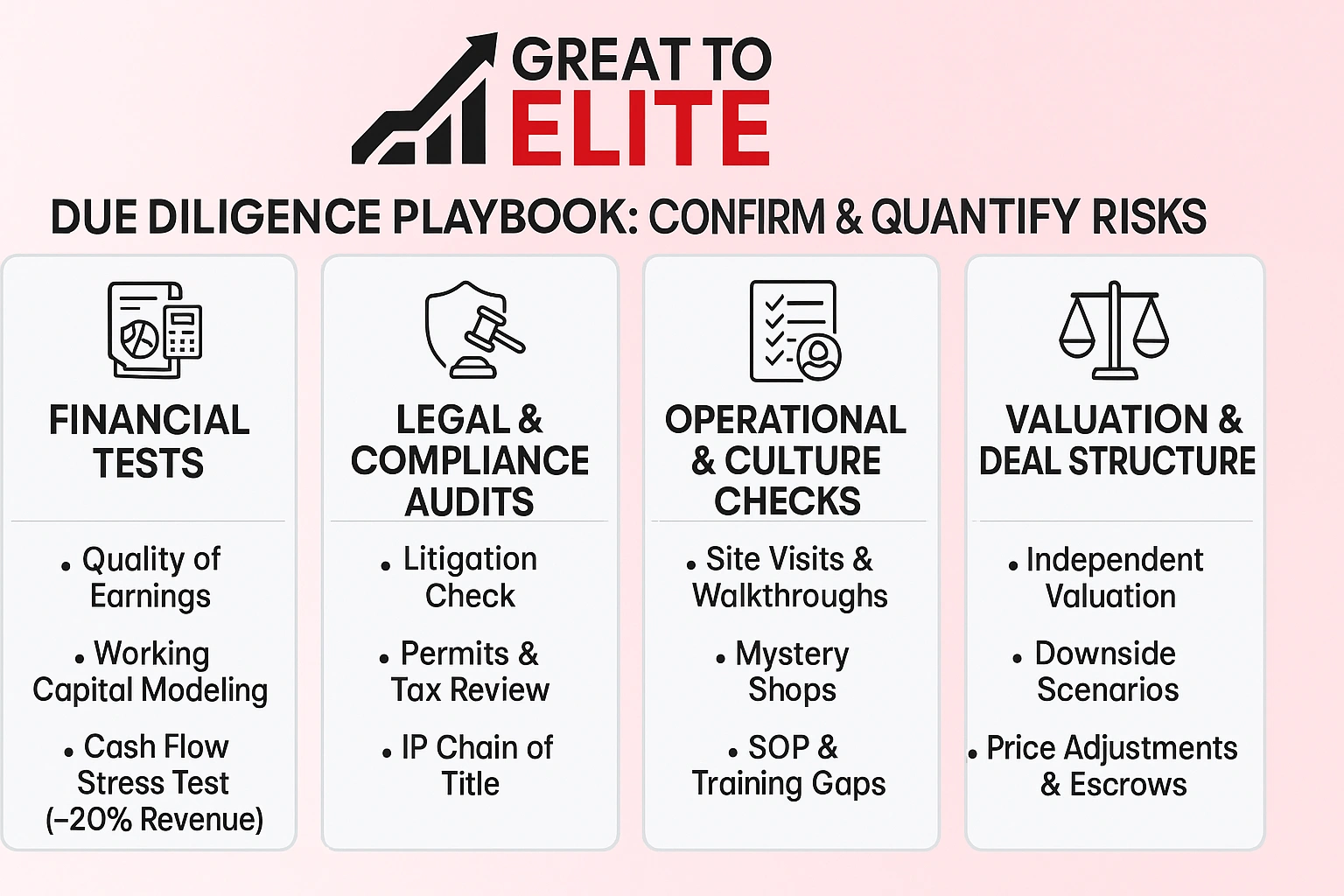

Due Diligence Playbook: How To Confirm And Quantify Risks

Begin with tests that force numbers and stories to align under pressure. Your goal is clear outputs: adjusted earnings, working capital needs, legal exposures, and operational fixes tied to cost and time.

Quality of Earnings, Working Capital, and Cash Flow Tests

Run a quality of earnings to separate recurring revenue from one-time items and to validate statements against bank and tax records.

Model working capital by season and stress cash flow with a 20% revenue dip. Output: normalized EBITDA, target WC reserve, and cash cushion required for purchase.

Legal, Compliance, and IP Audits

Review litigation, tax history, permits, and IP chain of title. Output: liability schedule, cure costs, and assignment gaps that must be fixed before close.

Operational Walkthroughs, Mystery Shops, and Cultural Fit

Perform site visits, ride-alongs, and secret-shop calls. Output: SOP gaps, training needs, and retention risks tied to estimated remediation time and cost.

Independent Valuations and Stress-Testing Forecasts

Commission an independent valuation and run downside scenarios. Map every finding to price adjustments, escrows, indemnities, or reps so buyers can structure the purchase defensibly.

Deal Structuring To Mitigate Red Flags

Translate diligence findings into deal mechanics that protect value and align payout with performance. Use clear pricing moves, contingent payments, and protections so you, as the buyer, only fund verified outcomes.

Price Adjustments, Earnouts, and Holdbacks

Adjust price for documented issues and add contingent earnouts tied to customer retention or revenue mix. For concentration risk, link payouts to retention of top accounts over 12–24 months.

Escrows or holdbacks sized to severity, commonly 10–15% to cover claim exposure.

Earnouts tied to KPIs (revenue, gross margin, customer churn) to bridge valuation gaps.

Indemnities, Escrows, and Reps & Warranties Insurance

Draft specific indemnities for identified legal, tax, or IP exposures. Use escrow releases on milestone verification and consider reps & warranties insurance for complex transactions.

Retention Plans for Key Staff and Customer Transition Support

Offer short-term incentives and require seller transition services when owners or key staff drive sales. This preserves relationships and reduces integration cost.

Instrument

Use Case

Typical Size/Term

Escrow

Known claim coverage

10–15% for 12–24 months

Earnout

Concentration or growth gap

12–36 months; KPI-based

Indemnity

Legal/tax/IP defects

Specific caps tied to issue

RWI

Seller insolvency or complexity

Policy covers deductible; limits vary

Practical rule: document covenants and revisit valuation after structure changes so the overall economics meet your return hurdles and lender needs.

How Great to Elite Helps You Avoid Bad Deals And Buy With Confidence

Great to Elite provides strategic support you can leverage right away:

Great to Elite partners with service-business buyers to uncover what numbers and narratives miss, then turns findings into actionable decisions.

Financial Diligence: deep reviews of statements, cash flow, working capital, and debt schedules to protect value and avoid overpayment.

Operational Audits: process mapping, tech-stack assessments, site walkthroughs, and staff interviews to uncover execution gaps that hurt performance.

Market & Competitive Research: independent analysis to validate demand, saturation, pricing power, and differentiation in your target industry.

Legal & Compliance Coordination: checklist-driven reviews to confirm licenses, taxes, contracts, and IP are transferable to your company.

Deal Strategy & Negotiation: risk-adjusted price, earnouts, escrows, and indemnities that protect value and upside.

Post-Close Playbooks: 30/60/90-day plans for people, customers, and systems so you preserve revenue and profit from day one.

If you want expert help evaluating targets or structuring smarter offers, book a call with Great to Elite and move from interest to confident acquisition.

Conclusion

When you start your review, map real risks that can destroy value before you sign.

Treat warning signs as prompts: quantify exposures, renegotiate terms, or walk away to protect capital and time.

Keep process discipline. Verify records, test market signals, and pressure-test the company story with independent checks. Convert findings into deal structure and post-close plans that preserve value.

Prioritize targets where issues are identifiable and fixable within your timeline and capital plan. Use experienced advisors to speed diligence, spot blind spots, and avoid overpaying in a competitive sale or purchase market.

FAQs

What early questions should I ask a seller to quickly uncover hidden risks?

›

Ask for the last three years of financial statements, tax returns, bank records, customer lists, and an explanation of how the owner spends a typical week. Early gaps, delays, or inconsistencies usually signal deeper issues that require pause.

How can I tell the difference between a fixable problem and a deal-breaking red flag?

›

Evaluate whether the issue can be corrected within 3–12 months at a reasonable cost. Fixable items usually involve documentation, process gaps, or outdated tools. Deal-breakers tend to be structural problems like customer concentration, unstable cash flow, legal exposure, or declining market demand.

How do I verify the seller’s claims without appearing confrontational?

›

Ask for documentation instead of opinions. Use neutral phrasing such as “Can you share the supporting files for this number?” or “Let’s walk through the data behind this trend.” Professional sellers expect verification and will not be offended by diligence.

What questions should I ask employees during diligence without alarming the team?

›

Prepare neutral, role-focused questions such as how work is assigned, which tools slow them down, and what customers ask for most. Keep questions operational, not transactional, and avoid discussing the potential sale directly to prevent morale issues.

How can I screen a business before spending money on full due diligence?

›

Request a basic data room containing financials, AR aging, customer counts, contracts, leases, and debt schedules. Review these for inconsistencies, concentration exposure, or unexplained adjustments. If the data room is sparse or disorganized, slow the process or step away.

What are signs that a seller may be hiding declining customer relationships?

›

Watch for short contract terms, frequent customer complaints online, minimal repeat work, reluctance to provide references, or sudden losses of top accounts. These often precede revenue drops that sellers try to hide with optimistic projections.

How do I check whether the company’s reported margins are realistic for the industry?

›

Compare gross margin, net margin, and labor ratios to industry benchmarks using trade associations, lender reports, and local competitor data. Large deviations without clear explanation point to misreporting, aggressive accounting, or operational inefficiencies.