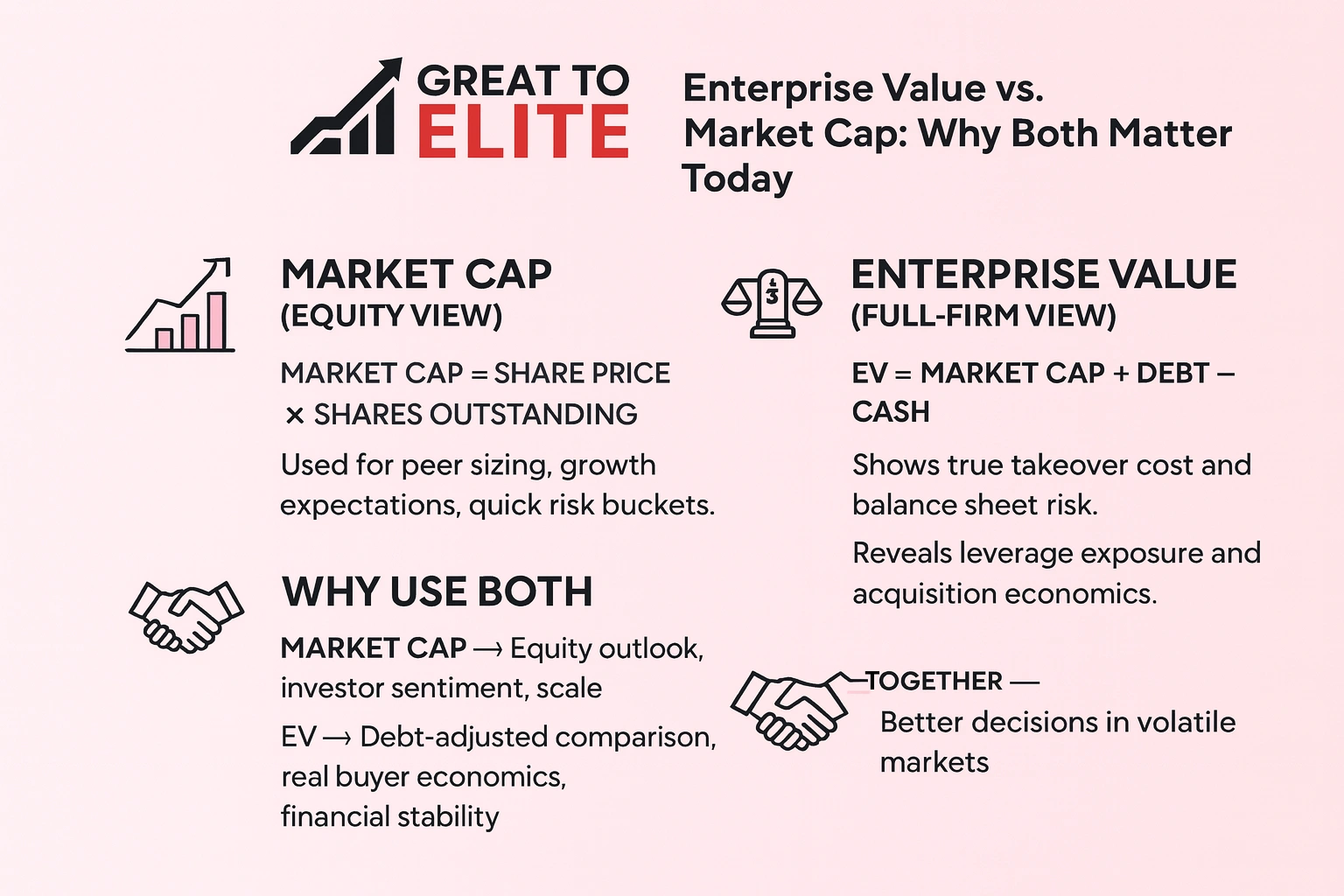

Enterprise value represents the total value of a company’s core operations. It captures what a buyer would effectively pay to acquire the entire business by adding market capitalization and total debt, then subtracting cash and cash equivalents. In other words, it reflects the full economic cost of ownership, since a buyer takes on the company’s debt but also gets access to its cash.

Market capitalization, on the other hand, shows the value of the company’s equity alone. It’s simply the share price multiplied by the number of outstanding shares. This figure tells you what the market believes the company’s equity is worth today, but it doesn’t account for debt, cash, or capital structure.

Key Takeaways

Market capitalization gives a fast size gauge using share price and shares outstanding.

The fuller measure adjusts that figure for debt and cash to capture total worth.

Use both metrics to compare a company to its peers and to spot hidden risks.

Formulas and ratios make the numbers actionable for investment or sale planning.

This guide will walk you from definitions to real use cases and practical checks.

Why Enterprise Value and Market Cap Matter

You are here to compare two commonly used metrics so you can judge how the market prices a company and how balance sheet items alter that picture. These numbers shape quick screening and deeper analysis alike.

Your Search Intent: Comparing Two Core Valuation Metrics

Market cap is the headline number many investors check to size a firm and sort peers by scale. It tells you how the equity market prices outstanding shares at a glance.

Enterprise value adds debt and subtracts cash to estimate what a buyer might pay to take control. That adjustment reveals financing risks and takeover economics that equity-only figures miss.

How These Numbers Influence Investment and Strategic Decisions

Use both numbers together to choose the right lens for your decision. Equity-only measures help with quick risk buckets and growth expectations.

Debt-and-cash-inclusive figures guide decisions about leverage, earnings impact, and acquisition pricing. They matter most in volatile periods when balance sheet strength changes outcomes.

Quick peer sizing and risk buckets with the headline number

Debt-aware comparisons that reveal hidden obligations

Better alignment of selection with your time horizon and tolerance

What Is Market Capitalization?

A simple multiply, current share price times outstanding shares, gives you a company’s market capitalization. This is the most common equity-level measure used to size firms on stock listings. You can verify it quickly when you check a quote page or a filing for the number of outstanding shares.

Definition, Formula, and Where to Find the Data

Market capitalization = current share price × outstanding shares. You will see this figure listed as a key statistic on most trading platforms and in public filings.

Share Price, Outstanding Shares, and the “Size” Signal

The headline number signals company size. A high share price does not always mean a large firm if the share count is low. Always check both inputs to confirm the result.

Large-, Mid-, and Small-Cap: Growth and Risk Profiles

Grouping firms by cap helps set expectations. Larger companies often show steadier revenue and lower volatility. Smaller firms may offer faster growth but carry bigger swings.

Quick check: multiply share price by outstanding shares to confirm the market capitalization.

Use the size buckets to match risk and horizon when you compare firms in an industry.

Remember the limitation: this measure omits debt and cash, so use it with other metrics later.

Metric

Formula

Primary use

Typical signal

Market capitalization

Share price × Outstanding shares

Quick company sizing

Equity market size

Inputs to check

Current price, share count

Verification on listings or filings

True scale and classification

Cap groups

Large / Mid / Small

Risk and growth buckets

Stability vs upside

Limit

Ignores debt & cash

Requires supplemental measures

Partial picture

What Is Enterprise Value?

To know what a buyer actually pays, you look beyond the stock price to include debt and cash on the balance sheet.

Definition, Core Formula, and Why Cash Is Subtracted

Enterprise value = market capitalization + total debt − cash and cash equivalents. This formula approximates the net cost to acquire a company's operations.

Cash is subtracted because excess liquidity reduces the net outlay a buyer would need. In an acquisition, that cash can be used immediately or returned to investors, lowering the effective purchase price.

Variations: Preferred Stock, Minority Interest, and Cash Equivalents

Some calculations also add preferred stock and minority interest to include non-common claims. Likewise, analysts subtract cash equivalents alongside cash for a cleaner, more liquid-adjusted figure.

Why EV Often Reflects a Company’s “True” Total Value

This measure blends equity value and financing claims so you can compare firms with different capital structures. Two companies with the same share-based size can show very different totals once debt and cash are included.

Total debt increases the measure because an acquirer assumes those obligations.

Subtracting cash and equivalents tightens the estimate of net cost.

Adding preferred and minority claims makes comparisons fairer across companies.

Component

Effect on EV

Why it matters

Market capitalization

Plus

Starting equity value

Total debt

Plus

Obligations an acquirer assumes

Cash & equivalents

Minus

Reduces net purchase cost

Enterprise Value vs Market Cap: The Key Differences

Different measures answer different questions. Market cap gives you a quick equity snapshot. Enterprise value adds debt and subtracts cash to show the net cost a buyer would face.

Equity-only perspective

Market cap reflects how the market prices common shareholders’ claim. It’s fast for sizing and screening companies, but it ignores obligations sitting above equity.

Debt-and-cash-inclusive view

Enterprise value layers in company debt and available cash. That makes it a closer proxy for acquisition cost and a clearer lens on capital structure and leverage.

Use market cap for quick peer sizing and sector scans.

Use enterprise value when assessing takeover cost, interest burden, or comparing firms with different financing mixes.

Watch company debt: high obligations can make equity appear cheap while raising real risk and cost for a buyer.

Metric

What it shows

When to use

Market cap

Equity-level size

Screening and quick comparisons

Enterprise value

Net takeover cost (equity + debt − cash)

Deal negotiations and capital-structure analysis

Combined view

Both lenses together

From screening to due diligence

Key Formulas, Components, and Data Sources

Start with simple math and reliable sources so your analysis stays consistent across companies and time.

Market Cap = Share Price × Outstanding Shares

Use this formula to get a quick equity size from live trading data. Check the current share price and the latest outstanding shares figure you can find in public filings or a trading feed.

Enterprise Value = Market Cap + Total Debt − Cash and Cash Equivalents

Apply this to fold in the company’s financing and liquidity. Total debt usually includes short- and long-term borrowings. Subtract cash and equivalents because those holdings lower a buyer’s net outlay.

Where Investors Pull These Numbers

Price and shares come from trading data and exchange records. Debt, cash, and equivalents appear on the balance sheet and in notes to financial statements.

Confirm inputs: reconcile price, share count, and balance-sheet items across filings and data feeds.

Document timestamps: record when you pulled each number for an accurate market value snapshot.

Variant adds: include preferred stock or minority interest when needed to compare companies with different claims.

Input

Source

Why it matters

Share price

Trading feed

Drives current market value

Outstanding shares

Company filing

Scales equity number

Debt & cash

Balance sheet and notes

Adjusts net cost for buyers

When to Use Market Cap vs When to Use Enterprise Value

Pick the metric that matches your decision. If you need a fast size check, use the headline equity figure. If you must judge takeover cost or compare firms with different financing, use the debt-and-cash adjusted measure.

Quick Peer Sizing and Risk Bucketing with Market Cap

Use market cap when you need speed. It helps you slot a company into large-, mid-, or small-size groups fast.

For top-of-funnel screens, this measure gives a directional read on volatility and broad risk. It is ideal when simplicity beats depth.

Comparing Companies Across Capital Structures with EV

Turn to enterprise value when debt and liquidity change the picture. This approach makes comparing companies fair across different financing mixes.

Use it for deeper valuation, acquisition scenarios, or industries that run higher leverage. Keep your peer set consistent so comparing companies yields clear insight.

Initial screens: choose market cap for speed and clarity.

Deeper analysis: choose EV for takeover cost and leverage checks.

Industry norms: favor EV when sector capital use skews comparisons.

Communicate which metric you used to stakeholders to improve transparency.

Use case

Best metric

Why it matters

Fast peer sizing

Market cap

Quickly groups company by size and risk

Leverage-sensitive comparison

Enterprise value

Reflects debt, cash, and takeover cost

Final valuation or deal work

Enterprise value

Better for pricing and capital-structure decisions

Interpreting EV/Market Cap and Common EV Ratios

Look at EV relative to the equity headline to see how leverage and cash shift a company's purchase cost. This ratio gives a quick read on whether total debt or large cash balances are changing the picture you get from the stock price.

Reading the EV/Market Cap Ratio: Debt Load and Risk Signal

When the ratio is high, it often signals heavier debt relative to cash. That points to more balance-sheet pressure and higher interest sensitivity for investors.

When the ratio is low, substantial cash or light borrowing can make equity appear more valuable than a simple price check suggests. Treat extremes as prompts to dig into company debt and cash equivalents.

Value and Cash Flow Lenses: EV/EBIT, EV/EBITDA, EV/Sales, EV/FCF

Use EV-based multiples to compare operational performance across firms with different financing. These ratios normalize for capital structure so comparisons are cleaner.

EV/EBIT ties total cost to operating earnings after depreciation and amortization adjustments.

EV/EBITDA focuses on operating cash before non-cash charges and is common for capital-heavy sectors.

EV/Sales helps when earnings are negative or inconsistent; it values revenue generation.

EV/FCF links total purchase price to actual cash generation available to investors.

Track these ratios over time. Improving margins, faster growth, or deleveraging should lower multiples or justify higher readings. Adjust for one-offs and how cash equivalents are treated in the accounts.

Ratio

Focus

When to use

Key signal

EV/Market Cap

Leverage vs equity headline

Quick balance-sheet screen

High = more debt; Low = more cash

EV/EBITDA

Operating cash proxy

Compare capital-intensive firms

Lower suggests cheaper operational price

EV/FCF

Actual cash generation

When cash flow matters most

Shows sustainability of valuation

EV/Sales

Revenue-based

Early-stage or loss-making firms

Helps assess top-line pricing

How Great to Elite Helps Businesses Turn Valuation Into Strategy

Move from numbers to action. You can translate the enterprise metrics you've learned into focused steps that grow company value and cash flow. Great to Elite helps you make that translation practical and repeatable.

Practical Support You Can Put to Work

Clarify Company Value: Align your understanding of enterprise worth with the story you tell customers and investors so operational gains reflect in company value.

KPI Dashboards: We build dashboards that track revenue growth, margin, working capital, leverage, and cash flow drivers tied to multiples and performance.

Pricing and Packaging: Optimize unit economics, packaging, and service mix to lift margins and predictability while reinforcing sustainable value creation.

Financial Modeling: Run scenarios for hiring, investment, and financing so you can prioritize moves that boost enterprise metrics and cash flow.

M&A Readiness: Prepare clean data rooms and metric histories so due diligence highlights strengths instead of raising questions.

Go‑To‑Market Systems: Establish repeatable acquisition and retention motions that create durable growth and support higher valuation.

Work With Great to Elite: If you want practical guidance to link analysis to outcomes, book a call with Great to Elite to translate valuation insight into decisive actions that move your business forward.

Conclusion

Use market capitalization as your fast check: the stock price times outstanding shares gives headline size and a simple cap for screening.

Then bring in enterprise value to fold in debt and subtract cash and cash equivalents. That adjusted total shows the likely acquisition cost and how leverage shifts the picture.

Watch extremes: a much higher enterprise value than market cap often signals heavy debt. A low or negative result can mean cash exceeds obligations and warrants deeper review.

Start with market cap, move to enterprise value, layer ratios like EV/EBITDA, and verify price, shares, debt, and cash from filings to make sound calls.

FAQs

What happens to enterprise value if a company issues new shares?

›

When new shares are issued, market capitalization typically increases because the share count rises. Enterprise value may or may not change depending on how the company uses the capital. If the funds add to cash, EV can stay flat or even decrease because the additional cash is subtracted in the EV formula. If the funds are used to pay down debt or invest in operations, EV adjusts accordingly.

Can enterprise value ever be negative?

›

Yes. Enterprise value becomes negative when a company’s cash and cash equivalents exceed the sum of its market capitalization and total debt. This situation is rare and usually signals distressed equity pricing, extremely high cash reserves, or unusual balance-sheet situations that deserve a deeper look.

Why doesn’t market cap show a company’s real acquisition cost?

›

Market cap only reflects what equity holders are worth at current prices. A buyer takes on the entire business, which includes debt obligations but also benefits from available cash. Market cap ignores both, so it cannot represent true takeover cost on its own. That’s why enterprise value is the standard for acquisition analysis.

Does market cap change throughout the day?

›

Market capitalization fluctuates constantly during market hours because its primary input, the share price changes in real time. Enterprise value, by contrast, updates less frequently because debt and cash data typically come from quarterly filings, not minute-by-minute trading.

Why do analysts prefer EV-based multiples over P/E for some industries?

›

P/E focuses solely on equity and can be distorted by leverage, tax effects, or accounting differences. EV-based multiples (EV/EBITDA, EV/EBIT, EV/Sales) compare operational performance to the full cost of the business, making them more reliable for leveraged industries, capital-intensive sectors, or companies with irregular earnings.

Can two companies with identical market caps have very different enterprise values?

›

Yes. Capital structure creates divergence. One company may hold significant cash, reducing its EV well below market cap. Another may have heavy debt, pushing EV far above its equity value. Looking at both metrics side-by-side reveals risk, leverage, and liquidity differences that market cap alone hides.

.webp)