Business exit strategy planning is the process of creating a structured, goal-driven roadmap for transferring ownership of a business. It goes beyond simply “closing” a company; it focuses on preserving value, reducing risk, and achieving personal and financial goals for the owner.

A well-designed business exit plan defines the timeline, methods, and steps for exiting the business, whether through a sale to an external buyer, an internal transfer to family or employees, a merger, IPO, or an orderly wind-down. It aligns the company’s financials, operations, leadership, and legal/tax arrangements to maximize value and ensure a smooth transition for all stakeholders.

Key Takeaways

Start early to protect value and increase buyer confidence.

Document processes and clean financials to boost market value.

Consider the full spectrum of paths from sale to succession or wind‑down.

Coordinate advisors for valuation, tax, and legal clarity.

Keep stakeholders informed to maintain trust during transitions.

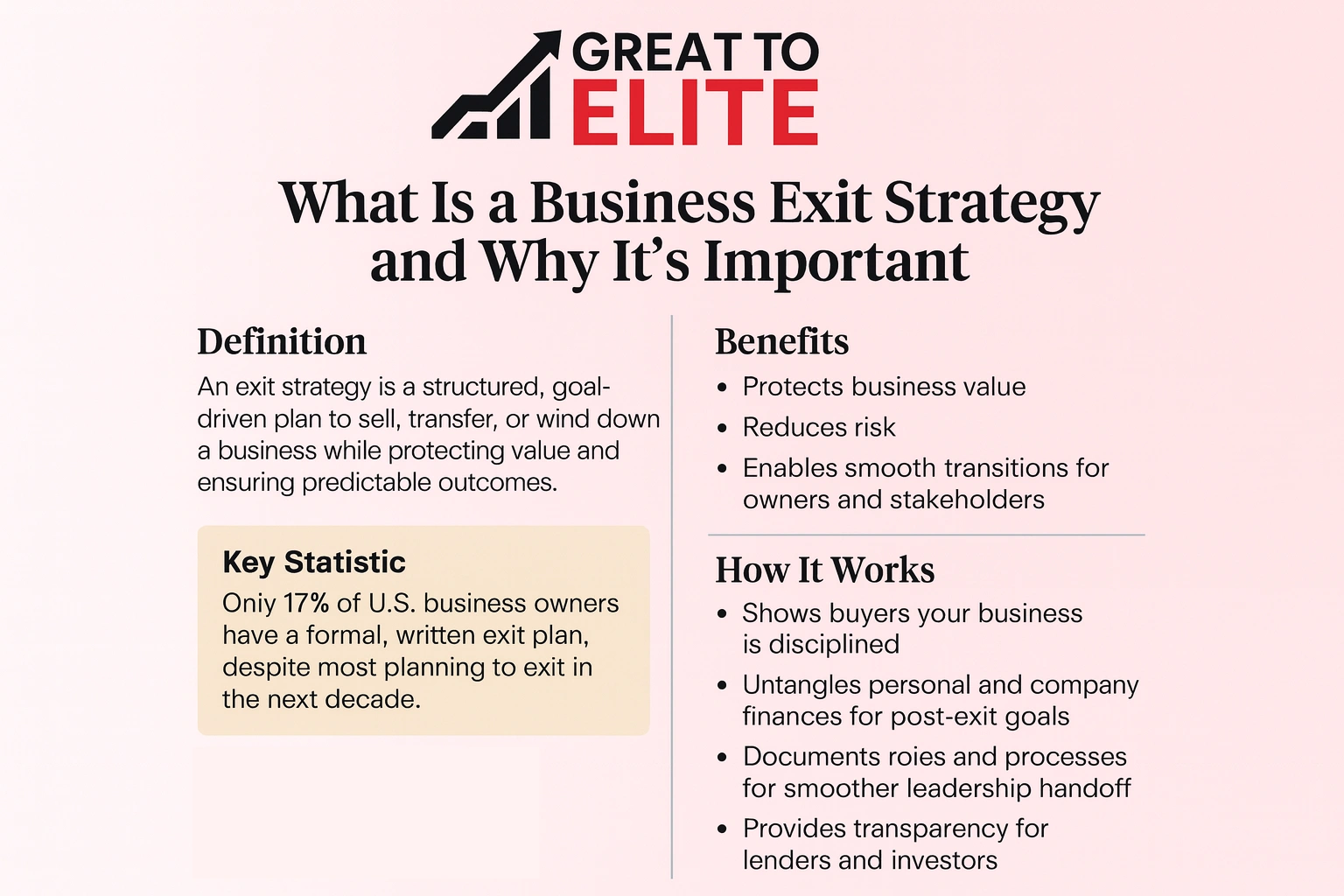

What Is a Business Exit Strategy and Why Is It Important

Preparing for a transition means more than closing doors; it means shaping outcomes that protect what you built. A complete exit strategy accounts for stakeholders, finances, and operations and maps the actions needed to sell, transfer, or wind down with control.

Research shows that only about 17% of U.S. business owners actually have a formal, written exit plan in place, despite most planning to exit their businesses within the next decade.

Defining Exit Strategy Vs. Simply “Ending” a Business

An exit strategy is a structured, goal-driven approach that sets measurable targets and timelines. It differs from shutting down because it preserves value and creates predictable results for owners and stakeholders.

Benefits: Protect Value, Reduce Risk, and Enable Smooth Transitions

When you document a clear plan, you:

Show buyers that your company is disciplined, which can improve terms and price.

Untangle personal and company finances so owners can reach post-exit goals.

Reduce reliance on you and document roles and processes for a smoother leadership handoff.

Give lenders and investors transparency about repayment paths and contingencies.

Use early tax and legal work to protect proceeds and preserve value.

Good timing and a thoughtful approach create more options in volatile markets and help make sure your post-transition life and finances align with your goals.

Set Your Goals and Vision for Life After the Exit

Picture the life you want after you transfer ownership, then work backward to make it real. Clear personal and financial goals should drive every choice in your plan.

Use a practical income rule: target roughly 75% of current income for post‑retirement needs, and subtract expenses the company currently covers (auto, insurance, travel). This shows your true cash needs.

Next, calculate an asset gap: compare current company value with retirement and liquidity needs. The gap tells you whether to work more years, boost value, or accept different proceeds.

Articulate personal priorities, lifestyle, location, family, and purpose, to align decisions with your future.

Set business goals that raise transferable value: recurring revenue, diversified customers, scalable ops, and leadership depth.

Define milestones in years for financial clean up, margin gains, and mentor successions.

Decide success criteria for deal terms, ongoing involvement, and risk retention.

Commit to a written plan that ties goals to milestones and advisors. That written road map keeps you focused and makes choices measurable as you move toward your next chapter.

Know Your Options: Common Exit Strategies Explained

Before you act, map the main options so you can match goals to the right type of transfer. Each option balances price, timing, control, and cultural impact.

Sell the Company: Strategic Buyer, Competitor, or Investor

External sales often produce higher proceeds and a faster sale. They can bring cultural shifts and may require you to stay short term to help integration.

Transition Inside: Family Members, Key Employees, or ESOP

Internal transfers keep culture intact but may need seller financing or phased buyouts. ESOPs move ownership via a qualified retirement plan using an independent trustee and a fair market appraisal.

Go Public or Merge: IPOs, Mergers, and Acqui‑Hires

IPOs offer capital but add heavy compliance and public scrutiny. Mergers or acqui‑hires speed growth or secure talent when your people are the main asset.

Close and Liquidate: When Winding Down Makes Sense

Liquidation converts assets to cash to settle debts. Options include gradual wind‑down or rapid asset sale; steps include dissolution filings, final tax returns, and required employee payments.

Compare external sale vs internal transfer on control, speed, price, and cultural fit.

Review deal types for employee buyouts, ESOP mechanics, IPO readiness, mergers, and liquidation paths.

Weigh how assets, contracts, and customer ties affect buyer interest and your leverage.

Build Your Exit Team and Timeline

Assemble a core group of advisors who will keep your interests front and center from day one. Name who leads internal work and who you’ll hire to cover legal, tax, and value issues.

Advisors You Need: Attorney, Accountant, Valuation, And More

Your advisory team should include an attorney for contracts and entity work, an accountant for tax and diligence, and a valuation expert to set baselines. Add a financial advisor for wealth guidance and a trust advisor for estate tools.

Assemble a coordinated team, attorney, accountant, valuation expert, financial and trust advisors, to cover legal, tax, value, and estate considerations.

Define roles and workflows so diligence materials, contracts, and tax work happen in parallel and save time.

Schedule valuation early to set baselines and discover value gaps you can close before going to market.

Recommended Lead Time: From “Exit‑Ready” To Deal Close

Create a master timeline that ties tasks to owners and meeting cadences. A 5–7 year horizon is ideal for complex transfers; 2–3 years is a practical minimum for most owners.

Map critical path items like quality of earnings, legal clean‑up, and governance updates that can stall a buyer if neglected.

Build an operations readiness plan to reduce owner dependence and show durable performance through processes and controls.

Prepare “exit‑ready” materials, financial packages, KPIs, contract summaries, and risk registers before buyer outreach.

Stage

Typical Time

Primary Focus

Preparation

2–7 years

Value gaps, ops, governance

Marketing & Close

3–6 months

Due diligence, contracts, tax

Contingency

Adjust as needed

Market shifts, health, timing

Assign internal project leads, set regular check-ins, and include contingency checkpoints so the plan stays strategy‑driven, not calendar‑driven. That approach keeps work focused and helps you protect value while managing time and risk.

Valuation Fundamentals: Understanding and Growing Market Value

A reliable valuation converts your financial story into a defensible price range buyers will accept. Buyers focus on normalized earnings, quality of earnings, asset base, and risk controls when they set offers.

Document recurring revenue, customer concentration, and margin trends. A clear quality‑of‑earnings analysis that normalizes expenses makes your numbers credible.

How Buyers Assess Value: Earnings, Assets, and Risk

Buyers evaluate adjusted earnings, asset efficiency, and operational risk. They reward predictable cash flow and penalize single‑customer reliance or weak controls.

Practical Levers to Increase Value Before a Sale

Reduce customer concentration and diversify channels and contracts.

Strengthen leadership depth to show the company runs without single‑person dependency.

Document processes and tighten controls to lower perceived risk.

Improve working capital turns and inventory efficiency to boost free cash flow.

Quantify pricing power and backlog to justify higher multiples.

Value Lever

Action

Buyer Impact

Timing

Recurring Revenue

Lock multi‑year contracts

Higher multiple for predictability

6–18 months

Leadership Depth

Promote deputies and document roles

Reduced key‑person risk

3–12 months

Asset Efficiency

Improve turns, cut excess inventory

Better cash flow, higher valuation

6–12 months

Quality of Earnings

Normalize expenses; fix anomalies

Stronger diligence outcome

3–6 months

Financial, Tax, and Legal Considerations You Can’t Ignore

Financial structure and legal safeguards determine how much you keep and how smooth the transfer will be. Choose terms that reflect your tolerance for risk, need for cash, and desire to retain upside.

Deal choices commonly include installment sales for steady cash, earn‑outs tied to future performance, or keeping a minority share to capture later upside. Internal transfers often use seller financing or leveraged buyouts.

Compare assets versus equity sale impacts on taxes, liabilities, and integration.

Plan entity‑specific tax moves so more proceeds qualify for favorable capital gains treatment.

Align payout timing and earn‑out metrics with what you can influence after closing.

Refresh buy‑sell agreements, set trust or beneficiary steps, and grant a power of attorney to protect ownership continuity.

Make sure diligence docs, contracts, IP assignments, and employment agreements are ready to reduce closing risk.

Consideration

Typical Effect

When To Act

Owner Impact

Installment Sale

Steady cash flow

Before negotiation

Defers tax; mitigates risk

Earn‑Out

Bridges valuation gaps

Set clear metrics

Ties payoff to performance

Minority Share

Retain upside

Post‑closing terms

Continued involvement possible

Governance Tools

Continuity and control

Years before transfer

Protects heirs and owners

Succession and Leadership: Choosing Who Will Run the Business

Leadership transitions succeed when skills, culture, and clear roles align. You must match mission and values to whoever takes charge so customers and staff see continuity, and a well‑defined succession plan helps ensure that alignment throughout the handoff.

Evaluating Successors for Skills, Fit, and Culture

Assess candidates, family members, key employees, or an external hire, against the competencies you need for future growth. Internal candidates may lack capital, so plan financing that does not overload operations.

Define the core competencies and leadership skills needed for tomorrow’s performance.

Evaluate each successor on experience, cultural fit, and appetite for ownership.

Structure training and shadowing so an employee or team can assume responsibilities confidently.

Design financing for insiders who lack capital and clarify governance roles after transfer.

Map relationships to protect customers and suppliers during the handoff.

Successor Type

Capital Need

Cultural Fit

Family Member

Low–Medium

High if groomed

Key Employee

Medium

High operationally

External Hire

Low

Variable

Document roles, decision rights, and a transition plan. Clear communication reduces misalignment and helps the owner keep trusted relationships intact through the change.

Operations and Due Diligence Readiness

Get your operations audit-ready so buyers or successors see a clean, repeatable record of performance. Organized files cut negotiation time and raise confidence in your company when you advance a transfer or wind-down.

Documentation Checklist: Financials, Contracts, and IP

Build a diligence vault with audited or reviewed financials, recent tax returns, customer and supplier contracts, and IP registrations. Reconcile tangible and intangible assets to your books to avoid closing delays.

De‑Risking Operations: Processes, Controls, and Compliance

Document core processes, order-to-cash, procure-to-pay, and record-to-report, so performance is repeatable without you.

Strengthen internal controls, policy manuals, and compliance evidence to reduce perceived risk.

Run mock diligence, fix unsigned contracts or lapsed licenses, and add cyber and employment checks tailored to your company.

Maintain an issues log with owners, actions, and deadlines to keep work on track as you approach exit.

Communicate Your Plan to Stakeholders

Open with investors and lenders so they hear your repayment path and the financial assumptions that support it. Start with numbers, scenarios, and timing to build trust and reduce surprises.

Investors and Lenders: Transparency and Repayment Paths

Share clear repayment or refinancing options and the forecasts that back them. Outline covenants, contingency funds, and who will sign for obligations.

Employees and Managers: Stability, Roles, and Retention

Tell managers early so they can stabilize teams. Be empathetic: explain roles, timelines, and any retention incentives you will use to keep key employees engaged.

Customers and Partners: Continuity and Relationship Handoffs

Introduce the buyer or new leadership to major clients and suppliers. Provide scripts and a handoff timeline so relationships remain intact and service levels do not slip.

Audience

Primary Message

Timing

Follow-up

Investors/Lenders

Repayment/refinance paths; forecasts

Before public announcement

Monthly updates; Q&A

Managers

Roles, authority, continuity actions

Immediately after funders brief

Weekly briefings; FAQs

Employees

Job expectations and retention terms

After manager brief

HR support; town halls

Customers/Partners

Continuity, contact points, introductions

Close to signing or at handoff

Personal outreach; transition docs

Document commitments and track sentiment across relationships.

Train spokespeople and supply consistent FAQs to make sure messaging aligns.

Define post-close support channels so ownership changes do not disrupt the company.

Timelines, Contingencies, and Market Conditions

Map your timetable so you control pacing and preserve optionality. Start with realistic horizons and decision gates that let you speed up or pause work based on events you can’t predict.

Typical Durations: Planning, Marketing, and Closing

Most owners treat 2–3 years as a practical preparation window and 5–7 years as ideal for complex transitions. From a prepared position, sales commonly take 3–6 months for marketing, diligence, and legal close.

Build milestones across those years so improvements in earnings quality and controls appear in the record. That makes offers stronger and due diligence smoother.

Contingency Planning for Health, Market, and Deal Shifts

Expect setbacks: health events, economic downturns, or sudden buyer withdrawals can move timelines. Create playbooks that protect value and keep options open.

Allocate buffer time for QofE, contract assignments, and approvals that often extend deals.

Pre‑negotiate third‑party consents and define fallback approaches like an internal transfer if conditions change.

Track market indicators, rates, valuations, and sector appetite, to pick the best moment to go to market.

Set decision gates that trigger timeline shifts and document lessons annually to update your exit plan.

Stage

Typical Duration

Primary Risk

Preparation

2–7 years

Owner dependence; governance gaps

Marketing & Close

3–6 months

Due diligence delays; buyer drops

Contingency

Adjust as needed

Health, market swings, regulatory holds

Keep operations “exit‑ready” so you can act when time and market conditions align. That discipline preserves value and improves your chances of the future you want.

How Great to Elite Helps You Plan and Execute a Successful Exit

Get hands-on support to raise value, reduce risk, and keep momentum toward the outcome you want. Great to Elite blends practical steps and experienced advisors to prepare your company for sale or an internal transfer.

Partner With a Team Focused on Value, Fit, and Execution

Clarity: You’ll translate goals into a clear plan, timeline, and target buyer profile that fits your market and company.

Valuation & Value Growth: You’ll receive an independent valuation and a value-growth roadmap tied to measurable KPIs.

Financial Readiness: You’ll get deal modeling, tax coordination, and forecasting to optimize net proceeds at sale.

Operations Upgrade: You’ll strengthen documentation, KPIs, and risk controls to improve diligence outcomes and growth prospects.

Succession & Deal Support: You’ll prepare successors, run outreach, and negotiate terms so the transfer preserves continuity.

Ready to move from great to elite outcomes?Book a call to discuss your goals and start planning a path that protects value and fits your life after the sale or transfer.

Conclusion

Disciplined preparation lets you control timing and capture the value your company earned.

Start early, document the plan, and tighten operations so you make sure valuation, tax, and legal work in your favor.

With coordinated advisors and clear communications, the path from preparation to close takes years, while closing often runs 3–6 months when you’re ready. That discipline produces stronger offers and a smoother transfer for owner and team alike.

Ready to act? Finalize your plan, align your team, and engage expert support so your next move turns years of work into realized value. Book the call in the prior section to begin.

FAQs

What is the difference between a business exit strategy and succession planning?

›

An exit strategy focuses on the planned transition of ownership to maximize value and meet personal or financial goals, whereas succession planning primarily ensures leadership continuity and prepares successors to run the business effectively. Both overlap, but succession is about people, exit strategy is about timing, value, and transaction.

How do I know the right time to start my exit plan?

›

The ideal time is as early as possible, typically 2–7 years before the expected exit. Starting early allows you to optimize financials, strengthen leadership depth, and close value gaps, reducing pressure and increasing leverage when offers arrive.

Can a small business exit strategy include partial ownership sales?

›

Yes. Owners can structure partial sales, earn-outs, or minority stakes to capture future upside while retaining some control. These options can be tailored to financing needs, tax planning, and succession goals.

How much does a professional exit strategy plan cost?

›

Costs vary based on company size, complexity, and advisors involved. A typical range is 1–3% of company revenue for full advisory services including valuation, legal, tax, and operational readiness, though DIY planning with selective advisors can lower costs.

How do I handle confidential information during the sale process?

›

Confidentiality agreements (NDAs) with potential buyers, secure data rooms, and staged disclosures are standard. Only share sensitive financials, contracts, and IP with vetted parties under strict legal protections to prevent competitive or market disruption.

How do I choose the right buyers for my business?

›

Consider strategic fit, cultural alignment, financing ability, and the impact on employees, customers, and stakeholders. Strategic buyers may pay more, while internal buyers or ESOPs preserve culture but might require financing support.

How do I measure the success of my exit strategy?

›

Success can be measured when you achieve pre-set goals: net proceeds, timing, ongoing involvement terms, cultural continuity, and post-exit lifestyle alignment. Use KPIs for value growth, leadership readiness, and operational independence to track progress before the exit.