The steps to buying a business are: follow a repeatable process: identify a target, determine value, negotiate terms, submit a letter of intent, complete due diligence, secure financing, and close with proper documentation. Typical diligence reviews at least three years of tax returns and current financial statements. LOIs often include an exclusivity period up to 90 days.

Expect clear timelines and key documents. Many deals mix debt and equity. Options include SBA loans, traditional bank loans, or retirement rollovers. Closings usually use escrow and formal purchase agreements reviewed by counsel.

This guide helps you evaluate fit, control risk, and manage the owner handoff so day one is stable. Great to Elite frames each decision around value and long-term growth for your company and protects the deal you create.

Key Takeaways

Use a repeatable process so you always know the next step and how choices affect ownership.

Due diligence confirms value, focus on financials, legal items, operations, and people.

LOIs typically include an exclusivity window; plan timelines around that period.

Financing can blend debt and equity; align capital with cash flow and goals.

Closing mechanics include escrow, formal agreements, and counsel review to reduce surprises.

Why Buying An Existing Business Can Be A Faster Path To Ownership

Stepping into an existing operation often gives you instant market presence. You inherit customers, trained staff, suppliers, and systems that start producing revenue right away. That head start cuts the time needed for trial and error.

Immediate cash flow lowers early uncertainty. Real revenue and historic records give you data for smarter choices instead of relying only on projections. In 2024 global M&A value hit about $2.6 trillion, and the U.S. drove more than half of that activity.

Established processes and supplier ties speed execution and preserve value.

Employees with institutional knowledge let you focus on growth rather than hiring from scratch.

Faster entry still carries risk: overpaying, hidden liabilities, or owner-dependent sales.

How to buy a company with focus: match the opportunity to your skills, budget, and timeline. Use thorough diligence to confirm value and durability before finalizing the deal.

Define Your Fit And Find Opportunities

Match what you do well with the types of companies you’ll consider. Clarify your skills, how hands-on you want to be, and the lifestyle you expect. This focus helps you shortlist businesses that fit your strengths and schedule.

Clarify Your Skills, Risk Tolerance, And Lifestyle Goals

Write down what you can run day-to-day versus what you’d delegate. Note your cash comfort level and timeline for returns. That makes it easier to judge industry fit and expected value creation.

Where To Source Deals: Brokers, Marketplaces, And Your Network

Search widely: online marketplaces, local brokers, CPAs, attorneys, franchise resales, and referrals from your network all surface different opportunities. Brokers can filter listings and help negotiate, so make sure their incentives align with yours.

Signals Of A Promising Target: Cash Flow, Customers, And Growth Potential

Look for steady or improving cash flow and clear paths to more revenue.

Prefer diversified customers, no single client should drive most sales.

Probe owner involvement; if the owner runs core work, plan a transition.

Signal

What It Shows

How You Act

Consistent cash flow

Operational strength and predictable returns

Model earnings and stress-test projections

Customer diversity

Lower concentration risk

Review top clients and contracts

Clear growth plan

Scalable opportunity in the industry

Estimate investment needs and payback

Owner-dependent operations

High transition risk

Negotiate training or earnouts for handoff

Evaluate Targets Before You Engage The Seller

Screening candidates early saves time and keeps your focus on viable deals. Before full engagement, set an initial checklist that filters opportunities fast. That checklist should flag simple disqualifiers so you don’t waste effort pursuing weak fits.

Understand Reasons For Sale And Owner Involvement

Ask why the sale is happening: retirement, health, or unresolved issues. Knowing motivation reveals what you may inherit and how long the owner will stay.

Confirm the owner’s role in daily operations. If one person runs core tasks, plan training or a phased handoff.

Early Red Flags To Watch For

Watch for the red flags when buying a business: inconsistent financial narratives, sudden drops in revenue, or heavy customer concentration. These often signal hidden liabilities or fragile demand.

Request high-level documents for quick screening: tax summaries, recent profit and loss, key contracts, and permits.

Speak with employees, customers, and neighbors when possible to verify claims about reputation and retention.

If you see signs of a rushed sale, pending litigation, or failing equipment, stop and reassess before advancing.

Screen Item

What It Reveals

Quick Action

Red Flag

Reason for sale

Motivation and transition support

Ask seller directly and note timeline

Vague or evasive answers

Financial snapshot

Revenue trends and expense anomalies

Compare last 12–36 months

Inconsistent statements

Customer mix

Concentration and retention risk

Review top clients and contracts

One client >40% revenue

Legal & assets

Possible liabilities and asset condition

Request key documents early

Pending suits or failing equipment

Steps To Buying A Business: From First Look To Closed Deal

Begin with a clear roadmap that maps every move from first look through closing. That roadmap keeps you strategic and helps you bring in advisors at the right moments.

High-Level Roadmap You’ll Follow

Identify target and run a preliminary valuation.

Negotiate headline terms and submit an LOI with an exclusivity window (often up to 90 days).

Perform due diligence, review at least three years of tax returns and core financials.

Secure financing (SBA, bank, seller finance), finalize purchase agreements, fund via escrow, and close.

Typical Timeline And Decision Points

Establish gates: initial valuation, offer range, LOI, diligence pass/fail, financing approval, and final agreements. Many deals stall during diligence when numbers don’t line up.

Keep communication clear with the seller to resolve issues quickly and preserve momentum. Build contingency time for lender underwriting, landlord consents, or third-party approvals.

Milestone

Purpose

Typical Duration

Key Owner

Preliminary valuation

Set realistic offer range

1–2 weeks

You and advisor

LOI and exclusivity

Lock negotiation window and outline terms

1–4 weeks

Buyer & seller

Due diligence

Confirm financials, legal, operations

30–90 days

Buyer, CPA, lawyer

Financing & close

Secure funds, finalize agreements, transfer ownership

2–8 weeks

Buyer, lender, escrow

Business Valuation Methods You Can Trust

A sound valuation turns past performance and future potential into a defendable price. Use methods that match how the target earns, owns, and competes so your offer rests on clear logic.

Income approaches: capitalized earnings and discounted cash flow

Start with earnings. Capitalized earnings works for stable profits; discounted cash flow fits growing or variable forecasts.

Translate normal owner-adjusted profit into a present-day value and stress-test growth assumptions.

Asset-based approach: tangible and intangible value minus liabilities

Use this when assets drive returns. Net tangible and intangible assets, less liabilities, often set the floor for price.

Market comparables: benchmarks and industry multiples

Look at recent sales of similar firms and apply multiples adjusted for size, margin, and local industry conditions.

Reconcile the three methods and weigh each by business model and risk profile.

Verify profit with clean statements and at least three years of tax filings before final modeling.

Adjust for customer concentration, owner reliance, team depth, and brand reputation.

Document each step so you can defend your price during negotiation.

Method

When Useful

Key Output

Income (Cap/D cf)

Stable or projected earnings

Present value of future cash

Asset-based

Asset-heavy operations

Net assets less liabilities

Market comparables

Active sale market

Benchmarked market price

Negotiating Price And Terms That Protect You

Protect value and define exactly what transfers and how you adjust the headline number. Start negotiations with clear structure: asset versus stock, and a workable purchase price framework. That helps you spot liability shifts and tax consequences early.

What’s Included: Assets, IP, Contracts, Inventory

List every asset, piece of IP, and assignable contract you expect to receive. Specify inventory counting methods and excluded items.

Adjustments, Earnouts, And Seller Support

Use working capital targets and inventory adjustments so the effective price at close matches expectations. Consider earnouts or seller notes to bridge valuation gaps while sharing downside risk.

Define inclusion schedules so the agreement mirrors your intent.

Clarify transition support: hours, duration, scope from the seller.

Negotiate reps & indemnities to address known and unknown liabilities.

Issue

Buyer Fix

Seller Option

Working capital

Target and true-up at close

Accept target or adjust price

Inventory

Count method and valuation

Agree on exclusions or buyback

Liabilities

Prefer asset sale to limit exposure

Offer limited reps or escrow holdback

Letter Of Intent (LOI) And Exclusivity

An LOI frames headline expectations so your teams can move quickly and with fewer surprises. Use this document to outline price, structure (asset or stock), timing, and key terms. Most LOIs grant an exclusivity window, often up to 90 days, so you can run focused diligence without competing offers.

Be explicit about which clauses are binding. Confidentiality, exclusivity, and access rights usually stick. Most economic items remain non-binding until you sign the final agreement.

Align the LOI with your financing plan and diligence scope. That keeps downstream documents consistent and reduces re-trading of core points.

Lock price, structure, and exclusivity so you can invest time in review with confidence.

Set timelines for information delivery, systems access, and third-party approvals.

Map a clear path for drafting the definitive agreement and assign responsibilities.

Clause

Purpose

Typical Duration

Buyer Action

Headline price & structure

Frame valuation and asset vs stock choice

Agreed in LOI; finalized at close

Confirm with advisor and lender

Exclusivity

Protect review period from competing bids

30–90 days

Use period for diligence milestones

Binding provisions

Confidentiality, exclusivity, access

Effective immediately on signing

Enforce confidentiality and request records

Timing & roadmap

Define deadlines and drafting responsibilities

Set clear turnaround times

Track milestones and escalate delays

Due Diligence Essentials You Should Not Skip

A thorough review can make or break your purchase, start with the right checklist. Rigorous due diligence often determines success; nearly half of acquisitions collapse during this phase when issues surface.

Financial Diligence: Tax Returns, Statements, And Cash Flow Trends

Request at least three years of tax returns, profit and loss, balance sheets, and cash flow reports. Reconcile tax filings with bank records and management statements to spot anomalies.

Legal And Contract Review: Leases, Litigation, And Assignability

Collect customer, supplier, and employment contracts, plus lease and property records. Confirm assignability and termination rights. Check for pending suits and contingent liabilities that may follow the deal.

Operations And People: Customers, Suppliers, Employees, And Systems

Validate AR/AP, vendor lists, equipment and inventory schedules, licenses, permits, and online sentiment. Look for customer concentration, owner dependence, and single-employee risk that can erode value post-close.

Risk Indicators That Commonly Break Deals

Red flags include missing or inconsistent financial records, unexplained revenue drops, undisclosed debt, or unwillingness to provide key documents. Document issues early and quantify impacts so you can reprice, add protections, or walk away.

Build a diligence plan that prioritizes documents and metrics that prove revenue quality and margin stability.

Review contracts for revenue triggers and assignability that change post-close economics.

Confirm liabilities such as payroll, sales tax exposure, and contingent obligations.

Financing Your Acquisition Without Derailing The Deal

Financing choices shape whether your deal closes on schedule or stalls under paperwork. Match funding to cash generation and your investment horizon so you can service payments without stretching working capital.

SBA Loans: Requirements, Timelines, And Fit

SBA-style loans often offer long terms and competitive rates but require detailed documentation and longer approval time. Plan application early and align lender milestones with diligence so closing time stays realistic.

Seller Financing: Structures And How It Pairs With Other Debt

Seller notes can bridge a price gap and keep your out-of-pocket lower. They also align incentives when the seller stays involved. Combine seller financing with bank or SBA debt when possible for balanced risk.

Bank Loans, Investors, And Friends & Family

Traditional lenders and private investors offer varied terms; friends can help but document agreements clearly. Each source affects control, repayment expectations, and future investor relations.

Using Retirement Funds And Personal Cash Responsibly

Retirement rollovers and personal cash reduce financing costs but preserve a cushion for tax and closing surprises. Keep reserves for operational needs after the transaction.

Coordinate lender deadlines with diligence and legal drafting to avoid last-minute delays.

Understand SBA paperwork so you can meet requirements early.

Document seller and friends arrangements to prevent future disputes.

Option

Typical Fit

Pros

Cons

SBA loan

Stable cash-flow companies

Low rates, long terms

Slow approval, heavy docs

Seller financing

Bridging valuation gaps

Lower upfront cash, aligned incentives

Seller risk retention

Bank / investor

Growth-focused targets

Flexible sizing, external oversight

Stronger covenants, possible dilution

Retirement / personal cash

Smaller deals or equity buy

No lender approval, faster close

Personal risk, tax consequences

Legal Structure, Agreements, And Closing Mechanics

Your chosen structure defines which liabilities you inherit and how the deal is taxed. Pick asset or stock transfer with clear expectations for tax, legacy exposure, and what moves with the company.

Asset Purchase Versus Stock Purchase: Tax And Liability Implications

Asset purchases often limit assumed liabilities and let you allocate purchase price among assets for tax benefit. They can require reassigning contracts and a lease transfer.

Stock purchases may be tax-favorable for the seller but can carry legacy obligations tied to the company. Match structure with lender and tax advice.

Critical Closing Documents And Compliance Items

Prepare these deliverables early so filings and consents finish before funding:

Bill of sale and IRS Form 8594 for asset allocation.

Non-compete, employment or consulting agreements, and IP assignments.

Assignments of contracts, lease consents, and permits.

Why Engaging A Lawyer And CPA Saves Time And Costly Mistakes

Engage counsel to review agreements, spot risky clauses, and coordinate escrow. A CPA will structure tax items and verify allocations.

Align closing checklists with lender and escrow requirements so funds transfer cleanly and you start day one with legal authority to operate.

Issue

Typical Document

Why It Matters

Action

Asset allocation

IRS Form 8594

Determines tax basis for assets

Prepare with CPA and include with closing package

Transfer of contracts

Assignment & consent

Ensures revenue continues post-close

Obtain counterparty consent before closing

Lease

Lease transfer or estoppel

Secures premises and prevents eviction

Coordinate landlord approval early

Seller obligations

Non-compete & consulting agreement

Protects goodwill and aids transition

Negotiate term, scope, and enforceability

Post-Close Transition Plan For Day-One Stability

Plan the first 30–90 days so operations stay steady and customers feel cared for. Start with an explicit, short day-one checklist that focuses on continuity, access, and clear communications.

Owner Handoff: Intros, Knowledge Transfer, And Systems Access

Schedule structured sessions with the owner for introductions, playbooks, and logins. Capture vendor contacts, SOPs, and recurring tasks in simple guides.

Hold short walkthroughs with key staff so each employee knows roles and immediate priorities.

Licenses, Permits, And Change Management With Staff And Customers

Confirm which licenses transfer and file for those that don’t. Notify regulators, landlords, and major customers early to avoid service interruptions.

Set a clear day-one plan that prioritizes continuity for customers and employees while you learn systems.

Schedule knowledge-transfer sessions and require written playbooks.

Coordinate filings for licenses and permits promptly.

Communicate early with staff and outline near-term priorities.

Pace change over time; safeguard service quality before altering pricing or process.

Track simple KPIs for the first 90 days to guide decisions.

Action

Timing

Owner

Intro calls with top clients

Day 1–7

You & seller

Systems and credential transfer

Day 1–14

You

License/permit filings

Day 1–30

Advisor / You

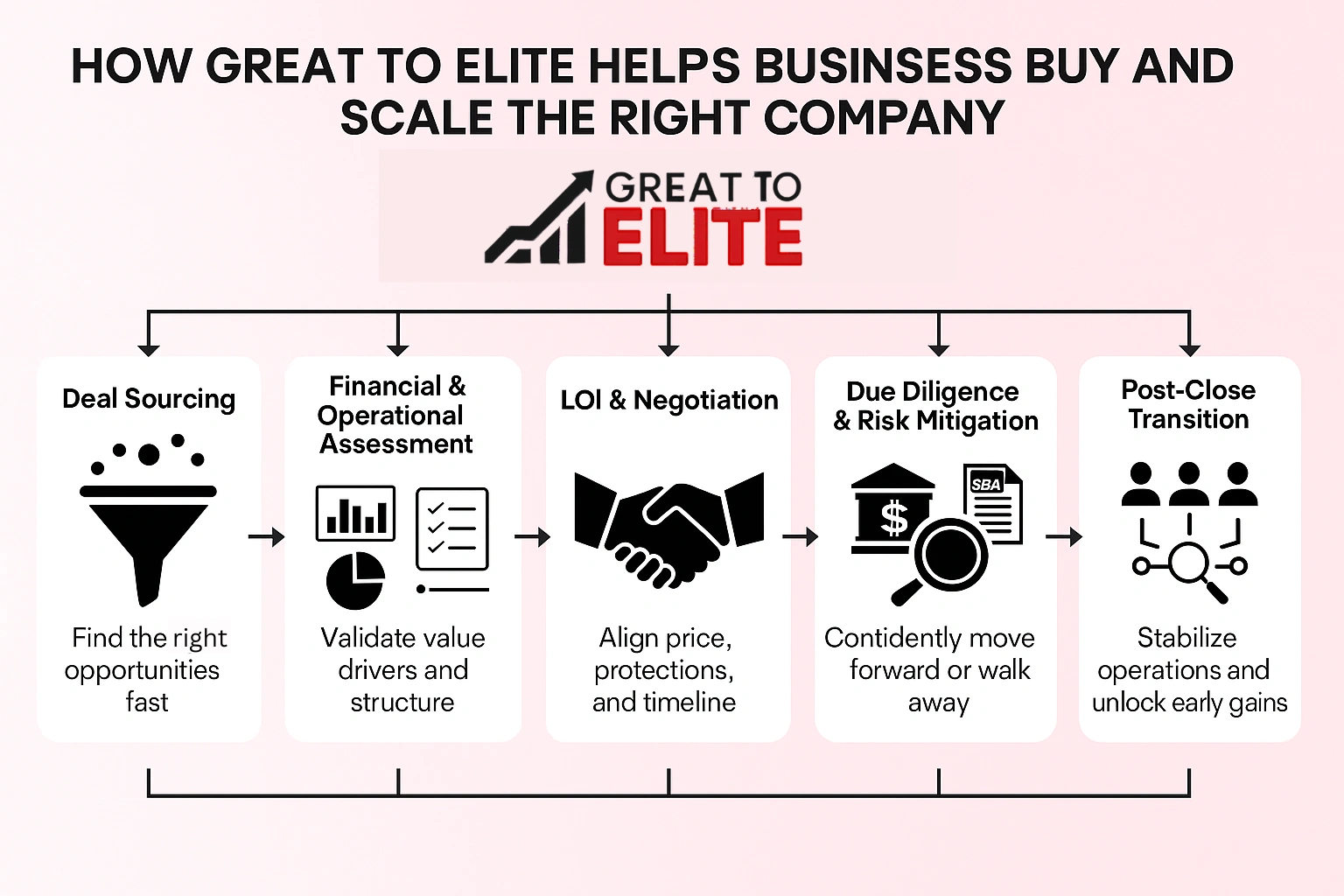

How Great to Elite Helps Businesses Buy And Scale The Right Company

A targeted approach shortens timelines and lowers deal risk, as it aligns criteria with real operational needs. Great to Elite works with you to find a purchase that fits your goals and cash flow targets.

We provide an end-to-end playbook tailored for service owners. That playbook covers sourcing, valuation, negotiation, diligence, financing, and the first days after close.

Deal sourcing tuned to your needs, with fast filters that show only matching targets.

Financial and operational assessments that validate value drivers and shape an appropriate purchase structure.

LOI and negotiation guidance that aligns price, protections, and the transaction timeline.

Diligence checklists, modeling, and risk mitigation so you move forward confidently or walk away when warranted.

Financing coordination and lender-read reviews to keep your transaction on track through funding.

Transition planning for the first days to preserve customers, stabilize the team, and unlock early gains.

Ready to pursue an acquisition or plan your next purchase? Book a call with Great to Elite and get an actionable plan for your next move.

Conclusion

Disciplined valuation and clear paperwork keep value intact. Frame price using verified statements and years of records, then set terms in a concise LOI or letter intent so the team can focus on diligence.

Run financial, legal, and operational reviews. Check contracts, lease assignability, property risk, and liabilities. Use an experienced lawyer for structure and tax guidance.

Align financing with cash flow and close with precise documents. Favor asset allocation when you need liability protection or consider stock for seller tax reasons.

On day one, protect customers and key employees, keep continuity, and use seller support for 30–90 days. Great to Elite helps you move through the purchase into stable growth.

FAQs

What size of business is realistic for a first-time buyer to target?

›

First-time buyers typically succeed with firms generating $300K–$2M in annual revenue because financials are easier to verify, operations are simpler, and financing is more accessible. Larger companies involve heavier diligence, negotiation complexity, and higher working capital needs.

How long does it usually take to find a business worth making an offer on?

›

Most buyers spend 3–12 months sourcing, screening, and reviewing deals before finding one that fits their skills, price range, and cash flow criteria. Timelines vary based on industry, search intensity, and clarity of criteria.

Do I need industry experience to successfully buy and run a business?

›

Not always. Many buyers succeed in new industries when they target companies with strong teams, stable processes, and limited owner dependence. If the business requires specialized knowledge, plan for training, advisory support, or a transition period with the seller.

Should I hire a business broker or buy directly from the seller?

›

Both paths work. Brokers help organize documents and manage communication, while direct deals may offer better pricing but require more buyer-led diligence. Choose based on your confidence in negotiating, evaluating risk, and managing the process.

What are typical closing costs when buying a small business?

›

Legal fees, lender fees, diligence costs, and filing expenses generally total 3–10 percent of the purchase price. SBA loans, escrow services, and lease transfers can add additional administrative costs.

How do I evaluate whether the staff will stay after the sale?

›

Review employee tenure, compensation, culture, and any key-person dependencies. During diligence, request anonymized role information and use transition agreements or stay bonuses to retain critical personnel.

What happens if the seller wants to stay involved after closing?

›

Many deals include consulting agreements or part-time roles for the seller during a defined period. Set boundaries for hours, responsibilities, compensation, and decision-making to prevent overlap or confusion for the team.

How do I know whether the business can support acquisition debt?

›

Model cash flow with conservative assumptions, including seasonality and margin pressure. Lenders typically expect sufficient debt-service coverage (often 1.25x or higher). Stress-testing projections reveals if the deal can carry financing without straining working capital.

What if issues appear late in due diligence, can I still renegotiate?

›

Yes. Material findings allow buyers to adjust price, request seller financing, add escrow holdbacks, or walk away. Document evidence and quantify financial impact so renegotiation remains grounded and credible.

How soon after buying a business can I start making major improvements?

›

Start with stability first. Most buyers wait 60–120 days before implementing major changes so they understand systems, staff capabilities, and customer expectations. Early, aggressive changes can disrupt revenue and morale.