Buying a company comes down to asking the right questions before you commit. You need to know why the owner is selling, how dependent the business is on them, and whether its financials actually match the tax returns. You must ask how revenue is earned, whether key customers will stay after the transition, and what liabilities, permits, or contracts may not transfer cleanly. You should question how EBITDA was calculated, what cash flow looks like after debt service, and how much working capital must remain in the business on day one.

You also need clear answers about operational stability. Ask who the key employees are, which systems run daily workflows, whether equipment needs major CapEx, and how the company acquires and retains customers. Finally, push for detail on deal terms: what the seller will guarantee, which risks they will indemnify, what support they provide in the first 90–100 days, and which consents are required before closing.

Key Takeaways

Start with buy vs build and assess M&A capability within your team.

Protect cash flow and validate financials, QoE, and working capital.

Weigh funding choices: cash, equity (dilution), or debt (capacity/interest).

Plan integration with TSAs and a 90–100 day operational plan.

Use targeted checks to spot red flags and avoid poor targets quickly.

Why It Is Important to Ask the Right Questions when Buying a Company

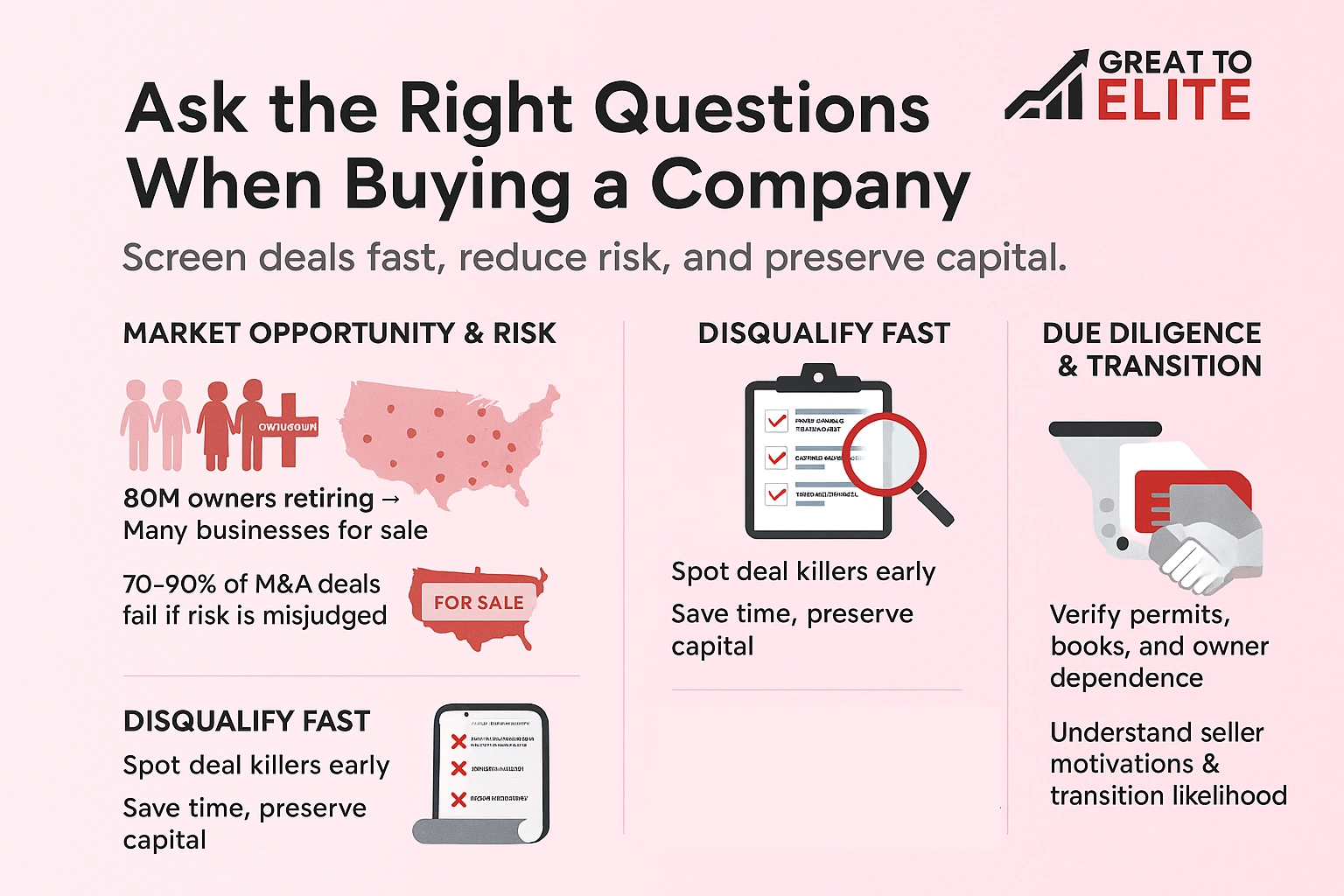

You are entering a market reshaped by retiring owners. Nearly 80 million baby boomers will exit ownership over the next decade, and that creates many businesses for sale across the United States. Even at the larger end of the market, 70%–90% of mergers and acquisitions fail to deliver their intended results, which shows how easily buyers misjudge risk, overpay, or underestimate integration challenges.

That supply brings variety. Some targets have clean books and transfer-ready permits. Others hide owner dependence, poor records, or unresolved legal issues. You need a fast, practical method to sort listings and save time.

Adopt a disqualify-fast mindset. Screen for clear deal killers early: concentrated customers, missing licenses, or seller opacity. That reduces wasted effort and preserves capital for sound opportunities.

You will use demographics and deal flow to justify a disciplined pipeline.

Due diligence now matters more: interest rates, labor markets, and debt capacity shift risk.

This guide structures conversations that reveal seller motivations and transition likelihood.

Clarify Your Deal Rationale Before You Search

Begin with a clear acquisition goal so your search stays focused and efficient. Define whether speed, cost, or strategic fit drives this move. Compare time-to-market gains against internal build timelines and expected expense.

Assess internal capacity. Map roles for sourcing, diligence, integration. Confirm who on your team can lead each phase and where you need outside experts such as legal, tax, QoE, or IT advisors.

Buy Versus Build: Speed, Cost, And Fit

Run a buy-versus-build checklist that weighs budget, skills, and timeline. Identify specific features you need: market access, tech, personnel, or contracts. Clear criteria make search filters useful.

Resourcing Your Acquisition Process

State a strategic reason: enter market, add tech, accelerate growth beyond organic reach.

Define fit by geography, services, culture, operating model.

Assign owners for sourcing, diligence, integration; confirm bandwidth.

Engage advisors where risk is highest: finance, tax, legal, compliance, tech.

Set screening rules tied to thesis and decision gates linked to data responsiveness.

Focus Area

Signal

Immediate Step

Speed

Need market entry within 6 months

Prioritize targets with existing customers

Cost

Build cost > acquisition premium

Model 3-year ROI

Fit

Mismatch in service or culture

Refine search filters, pass early

Resourcing

Core staff overloaded

Hire external diligence team

Funding The Purchase And Working Capital Needs

Deciding how you will finance the transaction alters control, cost, and post-close risk. Review funding choices early so your team can model outcomes and protect near-term liquidity.

Cash, Debt, or Equity: What Fits Your Risk Tolerance

Cash reserves buy speed and control but reduce cushion for operations. Equity reduces cash outlay but dilutes ownership. Debt preserves equity but adds interest and covenant risk tied to consolidated capacity.

How Much Net Working Capital Should Transfer

Net working capital typically equals cash + accounts receivable + inventory − accounts payable − accrued expenses. Secure recent bank balances and full debt schedules during due diligence and confirm the working capital peg in the purchase agreement.

Stress-Testing Liquidity Post-Close

Model conservative scenarios that include debt service, seller notes, earnouts, and integration costs. Identify off-balance-sheet liabilities, payroll timing, insurance, and tax obligations that could strain cash in the first 90–100 days.

Compare paying with cash versus using debt or equity, weighing control and cost of capital.

Negotiate seasonality adjustments and a clear working capital adjustment mechanism.

Request bank statements and debt schedules to validate near-term liquidity and covenants.

Funding Source

Primary Benefit

Main Risk

When It Fits

Cash reserves

Speed, no dilution

Reduced operational cushion

High confidence in statements and short integration

Equity

Preserves cash

Ownership dilution, higher long-term cost

When growth upside outweighs price of dilution

Debt

Maintains control

Interest and covenant pressure

Stable cash flows and covenant headroom

Questions To Ask When Buying A Company

Begin with core screening that exposes fatal flaws quickly and clearly. Use a short script that forces transparent answers on ownership dependence, legal exposure, and license transferability.

Disqualify Fast: Red Flags And Walk-Away Triggers

Refusal to share litigation history, client concentration data, or recent tax returns signals risk. Treat inconsistent bank statements and mismatched schedules as integrity issues.

Owner-dependent revenue or non-transferable permits are immediate triggers. Poor online reputation or unresolved compliance gaps often multiply integration costs.

Map Questions To Your Investment Thesis

Score each answer against market fit, scale, margin profile, and cultural alignment.

Set numeric walk-away thresholds for churn, largest-customer share, and deferred maintenance.

Require timely records; delays or changing stories reduce deal confidence.

Track every response in a central log to keep your team decisive and transparent.

Red Flag

Why It Matters

Immediate Action

Opaque legal history

Hidden liabilities can destroy value

Pause diligence; require full disclosures

Owner-dependent revenue

Loss risk after close

Insist on transition support or seller note

Non-transferable permits

Operational halt risk

Confirm transfer path or walk away

Data inconsistencies

Signals unreliable records

Delay offer until validated by QoE

What Are The Seller's And Business History

Learn the seller’s motive and how that story affects deal risk. A clear reason, retirement, relocation, or health, often lowers transactional friction. Financial distress is a red flag and changes diligence priorities.

Why the owner is selling and how long they’ve operated

Understand motive and tenure

Confirm when the business began and count meaningful years in operation. Longevity signals stability; short tenure can mean rapid change or higher upside but also more risk.

Ownership structure, litigation, and culture fit

Map structure, legal history, and team fit

Verify owners, investors, and decision-makers whose consent matters. Request a list of past and current lawsuits and evaluate successor liability risk.

Request references from key partners or customers to corroborate the seller narrative.

Screen for owner-centric relationships that may not transfer under new leadership.

Assess culture signals: turnover rates, communication style, and shared values that affect integration.

Focus

Why it matters

Action

Motive

Signals near-term transition risk

Validate credibility; model impact

Years operating

Indicates stability or growth stage

Adjust valuation and integration plan

Litigation

Possible hidden liabilities

Require disclosures and indemnities

What Are the Financial Statements, Tax Returns, And Earnings Quality

Gather complete financial history first so you can spot seasonality, one-offs, cash flow gaps, and revenue leaks. Secure the last three to five years of financial statements and current-year records. Reconcile those records against filed tax returns to verify reported income and profit.

Revenue, Profit, And Cash Flow Trends

Analyze sales patterns, gross margin, and net profit each year. Watch for volatile months and items that inflate cash. Confirm recurring revenue streams and separate one-time gains.

Debt Schedules, Liabilities, And Bank Balances

Obtain full debt schedules, covenants, maturities, and guarantees. Review bank statements to reconcile reported cash and spot undisclosed liabilities.

Tax Compliance: Returns, Liens, And Settlements

Collect income and sales tax returns for the past three years. Check for liens, settlements, payroll, and excise filings that could create post-close exposure.

Quality Of Earnings And Normalized EBITDA

Commission a QoE to normalize EBITDA and remove non-recurring items.

Reconcile accounting policies and flag aggressive treatments.

Use findings to model realistic profit under new ownership.

Document

Why It Matters

Immediate Action

Financial statements

Show trends, margins, cash

Reconcile to tax records

Bank statements

Validate liquidity

Match balances to books

Debt schedule

Reveals covenants and maturities

Assess refinancing risk

Tax returns

Confirm filings and liabilities

Search liens and settlements

Valuation And Price: Are You Paying Fair Market Value

Anchor your offer in data. Review income, balance, and cash flow statements. Check performance over recent years. Use facts, not guesses, when you value a business.

Methods: Multiples, DCF, Comparables, And Asset Value

Use profit multiples, discounted cash flow, comparable sales, and asset-based approaches. Each method reveals a different side of a business. Triangulate across methods to avoid single-point bias.

Benchmark against recent sales while adjusting for growth and capital needs.

Test sensitivity for margin compression, revenue shocks, and interest changes.

Validate QoE normalizations against your model inputs and statements.

Include CapEx, working capital, and integration costs when moving from enterprise value to cash needs.

Pressure-test management forecasts versus industry and documented track records.

Benchmarking Against Recent Sales

Approach

When It Helps

Key Adjustment

Multiples

Stable profit history

Growth and margin

DCF

Reliable cash forecasts

Discount rate

Comparables

Recent sales in industry

Scale and management

Ensure the final price fairly reflects risk allocation in the deal terms. Your company will then buy a business at a defensible value.

What Are the Day-To-Day Operations, Team, And Processes

Map daily routines and handoffs so you see where value gets created and where it stalls. That view guides hiring, integration, and short-term plan adjustments after close.

Org Chart, Employment Agreements, And Recent Workforce Changes

Obtain the org chart and headcount by function. Identify key roles and retention risks you must cover post-close.

Review employment agreements and compensation structures. Note layoffs or material workforce changes in the last 24 months for compliance and morale signals.

Products/Services, IP, And Production Workflow

Request a full product and services list and verify IP protections, trademarks, or patents. Confirm ownership and enforceability.

Document the end-to-end workflow. Map dependencies, handoffs, and single-point failures that could break customer commitments.

Facilities, Equipment Condition, And CapEx Needs

Inspect facilities, equipment, fixtures, and vehicles. Assess maintenance practices and immediate CapEx that the business will need.

Quantify costs to bring critical equipment to reliable standards and test whether current processes can scale without harming quality.

Workstream audit: product list, IP proof, and workflow diagrams.

Asset review: facility walk-through, equipment condition, and CapEx estimate.

Who Are the Customers, Sales Engine, And Churn Dynamics

Map who pays you and how stable those relationships are. Request a customer list that shows revenue by client and flag anyone over 15% of total income. That simple inventory reveals concentration risk quickly.

Top clients, concentration risk, and contracts

Review each major contract for term length, renewal mechanics, assignment clauses, and pricing protections. Note clients whose loss would cut income significantly and plan retention terms or earnouts to cover that risk.

Go-to-market, quote-to-cash, and CAC/ROI

Document lead sources, conversion rates, and the quote-to-cash flow. Measure CAC, average deal value, and marketing ROI to see whether growth is repeatable and cost-effective.

Churn trends and reputation signals

Analyze churn over the last two years and list drivers: competition, service gaps, or pricing. Check online reviews, refs, and NPS-style feedback to assess market perception post-transition.

Concentration: quantify top-5 client share and scenario-test loss impact.

Contracts: capture assignment & renewal language that affects transferability.

Sales engine: map funnel stages and key conversion metrics.

Finance: validate CAC and ROI against lifetime value.

Operations: audit billing, invoicing, and collections for bottlenecks.

Check

Why it matters

Next step

Top-customer share

Signals income vulnerability

Require retention plan or price adjustment

CAC & ROI

Shows acquisition efficiency

Validate with channel-level data

Churn trend

Predicts revenue sustainability

Investigate root causes and remediation

Who Are the Suppliers, Partnerships, And Competitive Landscape

Catalog every partner and supplier so you can measure continuity risk before closing. Gather the full vendor list, key terms, and notice periods. That lets you spot suppliers whose loss would halt production or services.

Supplier Contracts and Continuity Risk

Obtain contracts and verify assignment rights, pricing protections, and termination triggers. Confirm whether critical supply agreements require third-party consent on transfer.

Assess supplier concentration. If one vendor supplies most inputs, prepare contingency sourcing and short-term stock plans to protect cash and service delivery.

Alliances, JVs, and Margin Impact

Map joint ventures, revenue shares, and governance rules. These arrangements can shrink margins or limit your control after close.

Model how renegotiation or exit costs change value and your integration plan. Identify partners whose consent or ongoing cooperation is mission-critical.

Competitors, Market Share, and Industry Outlook

Map the competitive set and estimate relative market share to pressure-test growth assumptions. Research near-term industry trends and supply-chain disruptors that could raise costs.

Verify assignment rights and notice periods in key vendor contracts.

Prepare supplier contingency and inventory plans for continuity.

Evaluate JVs for margin dilution and decision rights impact.

Benchmark competitors and industry trends to adjust your plan.

Identify post-close procurement renegotiations that can unlock value.

Focus

Risk

Action

Supplier concentration

Supply interruption

Source backups, stock buffers

JV terms

Limited control, shared profit

Negotiate exit or governance rights

Market share

Competitive pressure

Adjust pricing and growth plan

What Is the Technology, Licenses, And Regulatory Compliance

Documenting systems and regulatory standing early prevents last-minute surprises at close. Catalog current tech and permits so you can scope migration effort, costs, and regulatory steps.

Tech Stack, Data Migration, And Integration Costs

Inventory the business tech stack, integrations, and data flows. Estimate migration hours, tool licensing, and security upgrades. Identify systems that need replacement or patching for your security standards.

Build an integration plan that sequences changes to limit disruption. Include testing windows, backups, and rollback triggers.

Permits, Licenses, And Transferability

Compile permits and licenses required for operations. Verify status with local regulators and confirm transfer steps and timing. Resolve compliance gaps before close to avoid fines or shutdowns.

Inventory tech, APIs, databases, and expected migration costs.

Flag systems needing upgrades for security or scale.

Confirm permit transfer rules and regulator contact points.

Assess compliance risks that could create liabilities after closing.

Focus

Risk

Immediate Step

Data migration

Loss or downtime

Run pilot migrations

License transfer

Operational pause

File transfer requests early

Regulatory gaps

Fines, liabilities

Remediate before close

What Are the Deal Terms, Risk Allocation, And Transition Planning

Set precise inclusions in the disclosure schedule before final signatures. That schedule locks what moves with the sale and what remains excluded from the purchase. Clear items here prevent disputes later and guide reps and warranties.

Disclosure Schedules, Inclusions, And Exclusions

Use the schedule to list contracts, leases, IP, and liabilities that affect value. Label excluded assets and carve-outs so there is no ambiguity at closing.

Reps, Warranties, Indemnities, And Covenants

Negotiate reps that confirm legal standing and accuracy of financials. Define indemnities, baskets, caps, and survival periods so responsibility for losses is clear.

Require covenants such as non-compete, non-solicit, and NDAs. These protect relationships, know-how, and goodwill after the purchase.

Seller Support: Training, TSAs, And Communication Plans

Secure seller support with a 90–100 day TSA and explicit SLAs for services. Include hands-on training windows and knowledge-transfer checklists.

Plan stakeholder announcements for employees, customers, suppliers, and lenders.

Make closing conditional on third-party consents and landlord approvals.

Document escalation paths for unresolved post-close issues.

Focus

Why it matters

Key term

Disclosure schedule

Prevents post-close disputes over included assets

Detailed inclusions/exclusions

Indemnity structure

Allocates financial risk for breaches

Baskets, caps, survival

Covenants

Maintains business continuity and value

Non-compete, non-solicit, NDA

Transition support

Reduces operational disruption after closing

TSA, training, SLAs

How Great to Elite Helps Service Businesses Buy With Confidence

Focused advisory cuts time-to-close and protects the value you just purchased.Great to Elite partners with buyers and their teams to build a clear plan for purchase, diligence, and integration. You get practical steps that reduce surprises and keep customers and staff steady through change.

Partner With Practitioners Who’ve Scaled Operations

Great to Elite supports your acquisition from strategy through hands-on integration. Each offering aligns with real-world operations and your growth goals.

Acquisition Strategy: You will build a precise buy-box and investment thesis so you filter better deals faster and align targets with growth goals.

Financial Diligence: You will interpret financial statements, tax returns, quality of earnings, and net working capital to validate cash flow and avoid surprises.

Operational Review: You will assess org design, processes, technology stack, and customer acquisition systems to confirm scalability and resilience.

Risk Mitigation: You will structure terms, covenants, and transition plans that protect cash flow and allocate risks appropriately.

Integration Playbooks: You will receive action plans across people, processes, and tech to integrate without breaking what already works.

Outcome: You reduce time-to-close, avoid costly mistakes, and buy businesses that thrive post-acquisition with confidence and clarity.

Next step:Book a call with Great to Elite to discuss your acquisition goals and receive a tailored action plan from a team that has scaled operations in the field.

Conclusion

The right checklist keeps you focused, reduces surprises, and speeds confident decisions.

Ask hard questions early and verify records, contracts, and cash before you move forward. If diligence is incomplete or price fails to reflect risk, be prepared to walk away. Bring legal and financial professionals into the process for fair terms and durable outcomes.

You will leave with clear steps: align your team, set a short transition plan, protect the future of the company, and translate findings into a realistic timeline that respects your time. Use this structured approach to buy business with confidence and create lasting value.

FAQs

What size of company should a first-time buyer target?

›

Most first-time buyers succeed when acquiring a business with stable cash flow, documented processes, and manageable headcount, typically firms generating $1M–$5M in annual revenue. Smaller businesses may be overly owner-dependent, while larger companies require more complex financing, stronger management experience, and deeper integration capabilities.

Should I sign an NDA before reviewing any detailed information?

›

Yes. Serious sellers expect an NDA before sharing tax returns, customer lists, contracts, or operational details. A proper NDA protects confidential information on both sides and sets expectations for handling sensitive data. Avoid reviewing detailed financials without one, it signals inexperience and may limit seller cooperation.

How do I determine whether the owner will support a strong transition?

›

Ask direct questions about their willingness to train, the time they can remain available, and their past experience transitioning responsibilities. Review how dependent the company is on the owner and whether staff can realistically assume those tasks. Strong sellers typically provide documented processes, customer introductions, and flexible support terms.

What should I know about earnouts before agreeing to one?

›

Earnouts tie part of the purchase price to future performance. They can bridge valuation gaps, but they introduce measurement disputes and integration constraints. Before agreeing, define metrics clearly (revenue, EBITDA, customer retention), establish reporting rules, and clarify who controls decisions that affect the earnout period.

How do I evaluate whether the company’s culture will fit my leadership style?

›

Interview staff informally, observe workflows, and sit in on meetings if possible. Look for communication norms, decision-making patterns, and expectations around pace and accountability. Culture fit impacts retention and integration costs, so assess whether your leadership approach will maintain morale and continuity.

What documents should I request before drafting an LOI?

›

Before you put anything in writing, request a financial overview, customer concentration summary, list of key contracts, details on licenses, and confirmation of major liabilities. You don’t need full diligence at this stage, but you do need enough data to avoid issuing an LOI you may later regret.

How can I assess whether the current staff will stay after I buy the business?

›

Look at historical turnover, tenure averages, compensation competitiveness, and employee sentiment. Request anonymized retention data and ask the seller about key employees’ career plans. Consider including retention bonuses or clarity on roles post-close to reduce flight risk.

What does a strong post-close communication plan include?

›

A good plan covers announcements to employees, customers, suppliers, and lenders within the first 24–72 hours of closing. It explains what will change, what will stay the same, and how support will continue. Consistent communication reduces uncertainty, preserves trust, and stabilizes operations during the first 90 days.