Buying a business starts with a clear financing plan, one that tells you exactly how much you can borrow, what lenders will approve, and how to structure the deal so the company’s cash flow can comfortably support repayment. Since 73% of business acquisitions require some form of external financing, most buyers must blend multiple funding sources from day one.

And while many people search for ways to buy a company with no money, the reality is that creative structures, like seller notes, earnouts, or partner equity, are what make low-cash or low-equity deals possible in practice. Financing a business acquisition follows a defined set of paths that combine debt, equity, and seller participation in different proportions depending on the deal.

Key Takeaways

You will learn a step-by-step approach for evaluating a target and selecting the right funding path.

Expect clear comparisons of SBA, bank, online, seller, and equity options plus typical down payment ranges.

See what lenders check early so you can align your plan, credit, and documents with approval criteria.

Get practical guidance on diligence, normalizing earnings, and validating historical performance.

Understand post-close cash priorities to stabilize operations and support growth.

Understanding Business Acquisition Financing Basics

Before you sign an offer, get clear on the funding basics that shape a successful acquisition. That clarity helps you pick terms that match your goals and the target's profile.

Buyer Goals, Deal Size, and Timeline

Define your objective, income replacement, growth, or platform building. Your goal sets debt tolerance, equity needs, and an acceptable repayment horizon.

Size the deal against normalized cash flow. This protects working capital and prevents overleveraging after closing.

Build a timeline that factors in underwriting. SBA reviews often take weeks to months; bank and online paths can be faster or slower depending on documentation.

How Lenders Evaluate Existing Businesses

Lenders weigh historical financial statements, operating expenses, assets, and customer base. Stable cash flow and predictable margins speed approval.

Expect requests for tax returns, valuation support, and personal financials.

Underwriters test revenue stability, seasonality, and working capital cycles.

Your credit, relevant experience, and a clear transition plan improve odds.

Underwriting Area

What They Review

Impact on Terms

Financials

3 years P&L, balance sheet, YTD statements

Interest rate, loan amount, documentation

Collateral & Assets

Equipment, real estate, inventory lists

Loan-to-value and guarantee needs

Qualitative Factors

Customer concentration, supplier risks, staff

Structure, covenants, contingency reserves

Tip: Share access expectations with the seller early so diligence stays on schedule and your closing date is realistic.

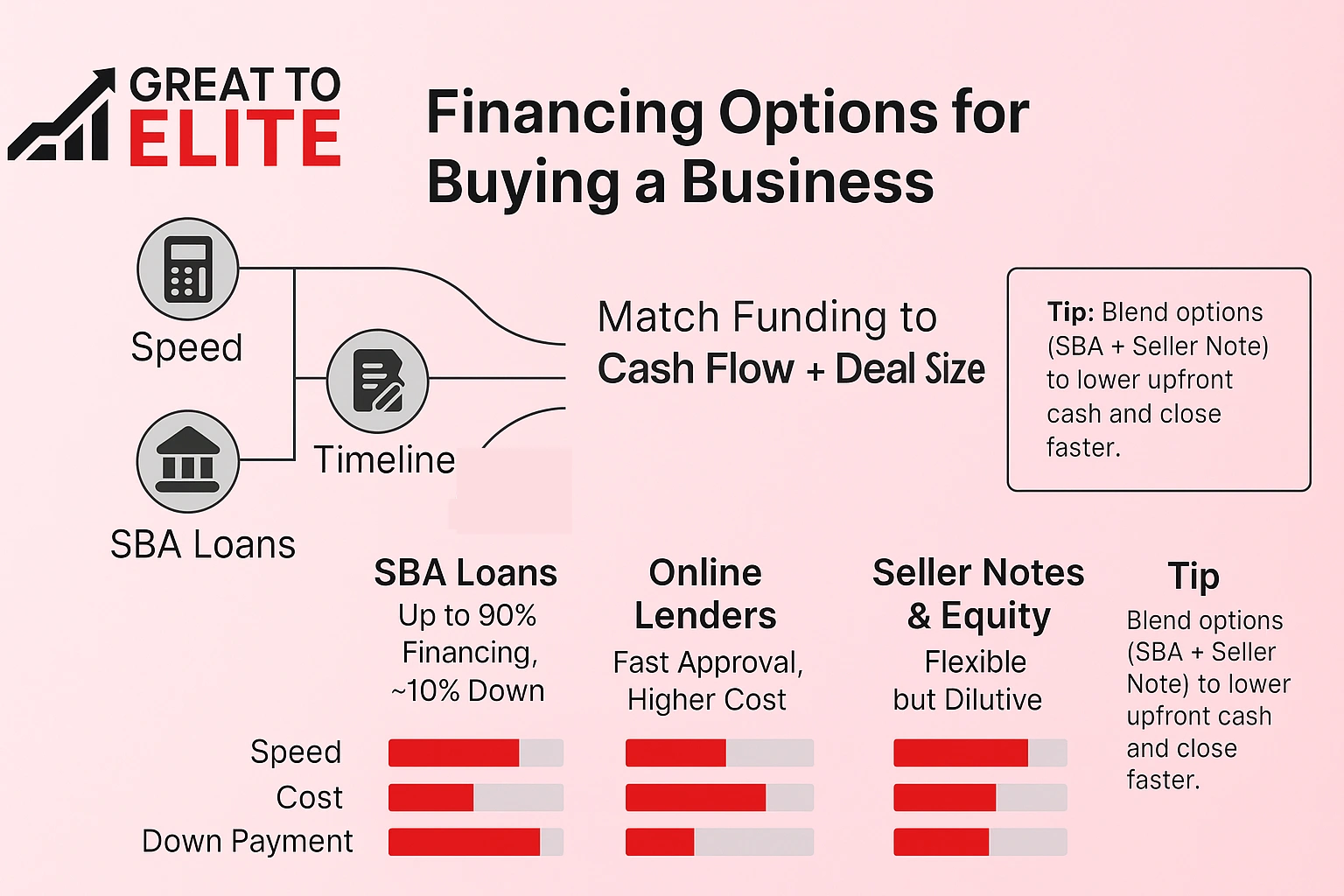

How to Finance Buying a Business: Core Options You Can Use

Select funding based on deal size, timing, and the target's cash flow. Matching lender rules with real earnings keeps monthly obligations realistic.

SBA 7(a), 504, and microloans: eligibility, equity injection, and timeframes

SBA loans can cover up to 90% of a purchase, with a common 10% equity injection. Expect underwriting measured in months; 7(a) loans may offer terms up to 25 years.

Bank and credit union term loans: collateral, personal guarantees, and rates

Traditional banks typically lend $100,000–$3,000,000 with one- to seven-year terms. Collateral and personal guarantees are standard, and down payments often sit at 20%–25%.

Online lenders and lines of credit: speed vs. cost trade-offs

Online paths approve faster but charge higher interest and shorter repayment terms. They work well for working capital or bridging gaps during closing.

Seller financing, LBOs, equity, and personal funds

Seller notes commonly cover 5%–60% of the price and may include performance-tied payments or covenants. Leveraged buyouts use the company's assets and future cash flow; debt assumption can reduce the purchase price but needs lender consent.

Equity capital reduces leverage for larger deals but means sharing control. Personal funds and retirement rollovers carry real risks; ROBS arrangements have shown higher lien and failure rates in some IRS reviews.

Compare interest, fees, and repayment terms across options.

Model worst-case cash flow to test coverage under stress.

Combine paths, for example, SBA plus a seller note, to balance needs and close faster.

What Lenders and Investors Will Ask For

Underwriters focus on documented cash flow, asset support, and an actionable transition plan. You should present a clear, organized package so reviewers can move quickly through each step of the review.

Financial Statements, Cash Flow, and Valuation

Provide at least three years of income statements, balance sheets, cash flow statements, and tax returns. Include year-to-date reports and AR/AP aging.

Attach a valuation narrative that ties income, market, and asset approaches. Show projections with base and downside debt service coverage.

Your Credit, Experience, and Business Plan

Submit a personal financial statement, recent tax returns, and a resume that highlights owner experience.

Include a concise plan that covers transition steps, staffing, and priorities for the first 90 days.

Collateral, Personal Assets, and Guarantees

List available collateral and disclose liens or encumbrances. Expect personal guarantees depending on program and loan size.

Factors

Requested Items

Why It Matters

Financials

3 years P&L, YTD, tax returns

Verifies earnings and repayment capacity

Assets

Equipment, inventory, real estate lists

Supports loan value and covenants

Owner

Personal statements, resume

Shows experience and reduces risk

Align your package with the chosen program's standards so the reviewer can process it without rework. That clarity speeds approval and lowers surprises in the process.

Comparing Costs: Interest Rates, Repayment Terms, and Total Price

Compare the true cost of each funding path so monthly and total outlays match your cash expectations.

Fixed rates give payment stability and make budgeting simple. Variable rates can start lower but expose you to increases that squeeze operating cash.

Fixed vs. Variable Structures

Fixed payments help you plan reserves and seasonal dips. Variable options may reduce initial interest but need sensitivity tests for possible rate spikes.

Down Payments and Purchase Price Mechanics

Include required equity injections in your close cash plan. SBA programs often ask for about 10% while conventional lenders commonly require 20%–25%.

Model full cost: interest, origination, appraisal, legal, and diligence fees annualized over the loan term.

Test amortizations: shorter terms raise monthly payments but cut total interest; longer terms lower payments but increase total price paid.

Seller notes can lower upfront cash but may add covenants or performance-based payments that affect future cash flow.

Shorter term, stable or variable rates, higher monthly burden

Online

Varies

Faster access, higher rates, shorter term raises cost

Seller Note

Reduces upfront price

Flexible structure; watch covenants and payment triggers

Make apples-to-apples comparisons and annualize fees, standardize prepayment assumptions, and model worst-case rate moves. Align the repayment schedule with the business’s cash generation and keep reserves for slow months.

Structuring the Deal: Blending Multiple Financing Options

A smart capital stack balances senior loans with junior notes or partner equity to preserve runway. This helps you meet program equity rules, improve coverage, and reduce cash at close. Keep designs practical and negotiable so lenders and sellers can sign off.

Common stacks that work in the U.S. market

Pair an SBA loans first-position tranche with a subordinated seller note to lower upfront cash and meet SBA equity requirements. The seller note can be amortized or performance-linked.

Alternatively, use a bank term loan plus investor equity. Equity lowers leverage and gives breathing room if cash flow is variable.

Repayment design: performance-linked vs. amortizing loan schedules

Performance-based payments align seller incentives with revenue stabilization. Amortizing term loans give predictable payments that ease budgeting.

Intercreditor clarity: define priority, remedies, and collateral for each tranche.

Amortization match: align loan life with asset life to reduce payment shocks.

Covenants: negotiate ratios you can meet and limits on extra debt or distributions.

Refinance plan: set payoff or refinance windows (often 24–36 months) for seller notes.

Assumption risk: secure lender consent before taking on existing debt.

Structure

Typical Coverage

Repayment Style

Primary Benefit

SBA + Seller Note

SBA covers majority; seller covers junior portion

Amortizing SBA; seller note can be contingent

Lower cash at close, strong coverage

Bank Term + Equity

Bank provides term loan; partners add capital

Amortizing bank loan; equity has no payment

Reduced debt service, better covenants

Seller Earnout + Loan

Lower upfront; earnout ties part of price to performance

Contingent payments plus regular loan amortization

Aligns incentives; protects buyer cash flow

Debt Assumption + Refinance

Existing obligations assumed, then refinanced

Subject to lender consent; later replaced

Can lower net price but needs lender approval

Step-By-Step: From Prequalification to Closing

Start with a clear checklist that moves your deal from prequalification through closing in defined steps. This gives you a predictable path and reduces last-minute surprises.

Assess eligibility and gather documentation

Prequalify with a lender to learn borrowing capacity and acceptable deal size. Collect three years of P&L, balance sheets, tax returns, and personal financials.

Prepare a concise plan, resume, AR/AP aging, and an asset list from the company.

Engage the seller and manage diligence

Set expectations for data access and monthly trend reports. Negotiate an LOI that covers price, working capital, and exclusivity.

Apply, negotiate terms, and satisfy conditions

Build lender-ready projections with debt service and sensitivity scenarios. Submit a full loan application and negotiate rate type, amortization, covenants, collateral, and guarantees.

Close and set up post-acquisition controls

Coordinate valuation, quality-of-earnings, and appraisals so conditions clear on schedule. Finalize equity injections, confirm fund flows, and secure insurance.

On day one, implement weekly cash forecasting and monthly reporting to protect runway and support early wins.

Mitigating Risks and Red Flags Before You Commit

Early detection of hidden liabilities gives you leverage and reduces surprise costs after closing. Running a lender-aware review helps you spot red flags when buying a business, focusing on financial history, operational handoffs, and obligations that may follow the sale.

Scrutinize revenue quality, margin trends, and customer concentration. Verify add-backs with source documentation and avoid accepting optimistic normalized earnings without proof.

Map operational handoffs: systems access, key staff roles, vendor terms, and supplier dependencies. Clear transition support from the seller lowers disruption risk in the first 90 days.

Identify lease commitments, pending litigation, warranty obligations, tax exposures, and any assumed debt.

If debt assumption is part of the deal, get explicit lender consent and model the assumed payment schedule.

Treat retirement account rollovers with caution; historical lien and failure rates argue for independent advice.

Stress-test cash models for loss of a major customer, delayed receivables, or sudden capex needs.

Risk Area

What to Verify

Impact

Financial History

Tax returns, P&L, validated add-backs

Affects underwriting, debt coverage, and valuation

Operational Handoffs

Employee retention, system access, vendor contracts

Controls early revenue stability and execution risk

Hidden Liabilities

Leases, litigation, warranties, assumed debt

Can create cash drains or lender objections

How Great to Elite Helps Businesses Acquire With Confidence

Make confident offers and align acquisition targets with realistic cash forecasts and lender expectations.Great to Elite guides you through financing choices and builds the materials lenders want. You keep control while improving odds of funding and a smooth close.

Why Partner With Great to Elite

When you need a partner that sharpens strategy and translates it into lender-ready deliverables, Great to Elite delivers a clear, proven process tailored for service firms.

Acquisition strategy: Clarify goals, target fit, and purchase ranges aligned to cash flow.

Financial modeling: Build projections, debt coverage, and sensitivity scenarios defenders for any lender.

Lender readiness: Organize documentation for SBA, bank, and online reviewers, reducing back-and-forth.

Deal structure: Compare blends like SBA plus seller notes or equity and see cash impacts side-by-side.

Operational transition: Get a plan for your team, systems, and cash controls that stabilizes day one.

Ready to move forward?Book a call with Great to Elite to assess your target, map a funding path, and get a concrete plan that helps you close with confidence.

Conclusion

Close with confidence when your package matches lender rules and the company’s cash profile.

Disciplined preparation and a clear capital stack speed closings and cut surprises. SBA loans can cover a large share with longer terms, while banks and online lenders trade speed, cost, and collateral differently.

Seller notes, leveraged buyouts, and debt assumption can lower upfront funds when backed by assets and steady cash flow. Treat retirement rollovers cautiously; IRS reviews show elevated risks.

Prioritize structures that fit the target’s earnings, validate historicals, and model interest and covenant shocks. If you want help building lender-ready materials, model scenarios, and shorten your path to ownership, book a call with Great to Elite.

FAQs

What credit score do I need to finance buying a business?

›

Most lenders prefer a credit score of at least 680, but stronger files, 700+ with low personal debt and clean payment history, receive faster approvals and better terms.

Can I finance a business purchase without putting any money down?

›

True zero-down deals are rare, but partial workarounds include combining a seller note with investor equity or assuming existing debt with lender consent; still, most lenders require a meaningful equity injection.

How early should I involve a lender in the acquisition process?

›

Engage a lender before issuing an LOI so you understand your borrowing capacity, required documents, and whether your target fits basic underwriting criteria.

Does the type of business I’m buying affect my financing options?

›

Yes. Lenders favor businesses with steady recurring revenue, diversified customers, and low cyclicality. Seasonal or project-based businesses may require larger reserves or stronger collateral.

Are asset purchases or stock purchases easier to finance?

›

Asset purchases are generally easier because lenders get clearer collateral and fewer inherited liabilities. Stock purchases require deeper diligence and may come with tighter covenants.

Can I use projected future revenue to qualify for a loan?

›

Lenders rely primarily on historical cash flow, not projections. Forecasts help support the story but cannot replace verified earnings in debt-service calculations.

How long should I expect underwriting to take from application to close?

›

Traditional bank underwriting often runs 30–60 days, SBA can take 45–90+ days, and online lenders may decide within days, but closing still requires completed diligence.

Can I finance working capital and growth investments as part of the acquisition?

›

Yes. Many lenders allow working capital, equipment upgrades, or marketing spend to be rolled into the loan if the business shows enough cash flow to support the additional debt.

What happens if the business underperforms after I close the loan?

›

You remain responsible for repayment. Underperformance may trigger covenant breaches, restrict distributions, or require immediate corrective plans, another reason to stress-test cash flow before committing.

.webp)

.webp)

.webp)