How to Buy a Company with No Money

How to Buy a Company with No Money

Natalie Luneva

November 27, 2025

You can buy a company with no money if you lean on financing, seller terms, and the target’s cash flow. Common options include SBA 7(a) loans backed by government lenders, seller financing with promissory notes and UCC liens, or creative capital from home equity and 401(k) loans. Each path has trade‑offs you must weigh.

Seller motivations like retirement or relocation often open room for flexible price and payment terms. Typical down payments sit near 20–30%, yet many deals negotiate lower upfront costs. Sale‑leasebacks can free real estate value, note U.S. leaseback activity topped about $17 billion, but poorly set leases can strain cash flow and add long obligations.

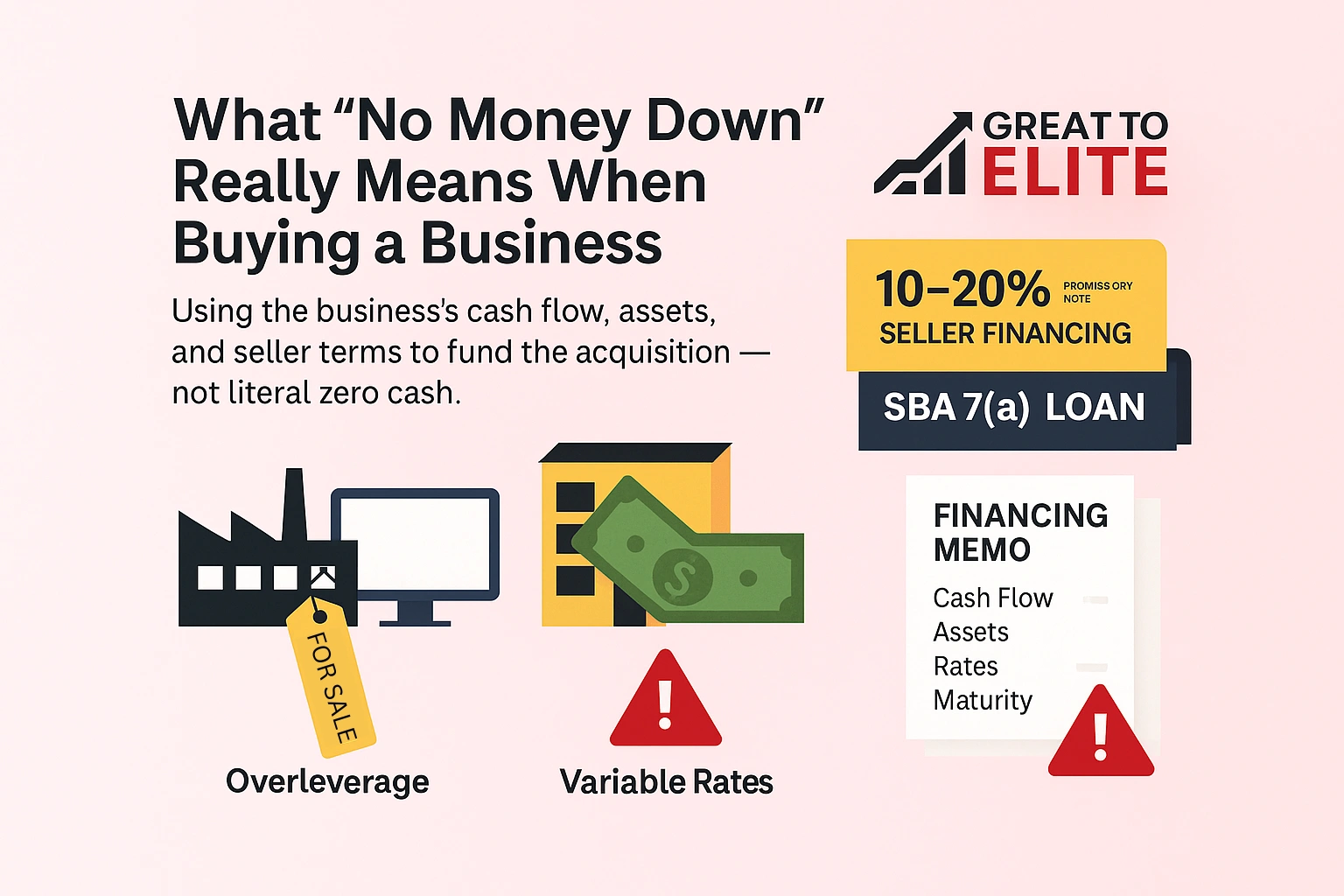

“No money down” typically means structuring payments so the target business covers debt service through its own earnings and assets. It rarely implies zero personal cash at closing. Instead, you piece together financing that leans on the firm’s cash flow, collateral, and seller terms.

Seller financing often fills the gap. Common arrangements include promissory notes covering 10%–20% of price, market-aligned interest rates, UCC liens on assets, and 3–7 year terms. Sellers accept this when it matches their exit timeline and price goals.

Government-backed loans, including SBA 7(a), favor profitable, existing enterprises. Lenders under small business administration rules focus on cash flow coverage, credit, and management experience rather than startup projections.

Assemble financing early and prepare a concise memo showing cash flow, assets, rates, and years to maturity. That memo strengthens your credit story for lenders and improves negotiating power with the seller.

Clarify your aim first: decide whether you want income stability, long‑term growth, or retirement acceleration. That clarity guides industry choice, deal size, and acceptable risk.

Define the primary financial motive early. Income buyers need predictable cash and margins. Growth buyers accept more risk for upside. Retirement seekers favor steady payouts and low management demands.

Choose revenue range, margin profile, and location that fit your cash needs. State if you will be a full‑time owner or a strategic, hands‑off leader.

Define must‑haves and deal breakers so you can filter opportunities fast and preserve precious time for the best fits.

Finding the right small business requires focused sourcing and a clear checklist for risk and upside. Map where reputable listings and brokers publish opportunities. Brokers streamline paperwork and access, while broad platforms let you compare many options quickly.

Use brokers when you need valuation help, lending readiness, and transaction coordination. Listing platforms help you screen volume and spot businesses that match your revenue and margin targets.

Common motives include retirement, relocation, illness, or a desire for a lighter workload. Align offers around those goals and propose terms that preserve staff and customers, this often improves negotiations and price outcomes.

Green lights include outdated technology or weak marketing where small investment lifts revenue. These are growth plays if core finances are sound.

Red flags include opaque financials, heavy customer concentration, problematic leases, or staffing issues that seem structural. Those raise credit and operational risk and may sink a deal.

Begin with a tight review of earnings, expenses, and receivables to confirm the business can support financing. Focus on normalized profit, recurring sales, and true operating costs. Lenders and sellers expect clear evidence that projected cash flow covers debt service and working capital needs.

Normalize revenue and remove one‑time items and owner perks. Check expense run‑rates and seasonal swings.

Inspect accounts receivable aging, inventory turns, and vendor terms to size working capital that must be funded at purchase.

Review debt schedules, rates, and covenants to see what liabilities reduce acquisition credit capacity.

Select valuation approaches, SDE multiples, EBITDA multiples, and comparable sales, and tie price to adjusted earnings. Factor in required capex and immediate working capital needs when you set the purchase price.

Inventory assets, equipment, vehicles, and IP, and note remaining useful life. Equipment and AR can serve as collateral to improve credit terms.

Map leases, renewal options, and escalations so occupancy costs do not erode margins after acquisition.

Interview key staff and review processes. If issues are fixable with training or systems, document those fixes in your memo and propose price adjustments, holdbacks, or contingencies for uncovered risks.

Action step: Convert findings into a concise investment memo that demonstrates value, debt service coverage, and collateral options for lenders and the seller.

Multiple capital paths can fund an acquisition when personal cash is limited, each with trade-offs in cost and control. Below are common financing routes and what they require from your plan, credit, and the target's cash flow.

Government-backed loans are issued by lenders and often reach roughly $5 million. They favor established, profitable targets and hinge on demonstrated cash flow and management experience.

Seller notes typically run 3–7 years with market-aligned rates. Expect UCC liens and performance covenants that bridge valuation gaps and reduce upfront payments.

Silent partners, angels, or equity investors can lower debt but dilute ownership. Traditional bank underwriting focuses on cash flow coverage.

401(k) loans and HELOCs add personal risk: 401(k) debt may accelerate if you leave employment and trigger taxes; HELOCs require monthly payments and income proof.

P2P and crowdfunding fill gaps but can be all-or-nothing or slow. Sale-leasebacks monetize real estate but can raise rent and stress cash flow; U.S. leaseback activity topped about $17 billion in recent reporting.

Follow a six-step path that turns goals and cash flow into a fundable plan. Begin with clear objectives and a concise funding memo that shows sellers and lenders you are credible.

Combine sources so payments match cash flow. Confirm which assets can back loans and document contingencies for diligence and financing approval.

Design offers that trade small price concessions for meaningful payment flexibility and lower risk. In practice, sellers will accept a higher nominal price when monthly obligations ease. Your job is to show how adjusted amortization or slightly higher rates create a win‑win.

Shift dollars between purchase price and payment timing. Longer amortization lowers monthly burden but raises total interest. Shorter terms cut total debt but increase near‑term strain.

Benchmark market rates and present a simple comparison for the seller and lenders. Demonstrate coverage ratios that show payments fit projected cash flow.

Openly discuss collateral: equipment, AR, or real estate can secure notes and improve credit access. Expect UCC liens on key assets and sensible limits on personal guarantees.

Set ceilings on guarantees and carve outs for ordinary business expenses so operations do not stall under debt covenants.

Include covenant triggers tied to cash flow, EBITDA, or revenue benchmarks. Early‑warning clauses allow temporary relief before defaults happen.

Build in financing and diligence contingencies, plus holdbacks or earn‑outs to bridge valuation gaps and align post‑close performance with seller payouts.

After the purchase, your focus shifts from transaction mechanics to steady operations. Finalizing the closing is only the start. You must protect cash, keep customers, and steady the team on day one.

Create a short transition timeline that lists owner shadowing, training sessions, and critical handoffs across the first 90 days.

Meet the team early. Share your vision, confirm roles, and document process owners so service quality stays stable.

Contact key vendors and customers personally. Confirm supply, pricing, and ongoing terms to avoid interruptions.

Work through contract assignments and bank account changes methodically. Update tax IDs and merchant processing before major billing cycles.

Coordinate escrow, verify all due diligence contingencies are satisfied, and only release funds when documents are complete.

Document lessons and refine processes as you settle into ownership. If you prefer a hands-off path, consider hiring an operator to run daily work while you monitor performance and protect the purchase.

Post-close momentum matters; Great to Elite designs short plans that protect cash and accelerate value. You get a focused program that turns early risk into steady growth. The approach centers on clear priorities and practical steps you can run from day one.

If you are planning an acquisition or recently closed, book a call with Great to Elite. We will map a plan that protects cash flow, aligns the team, and builds immediate momentum for lasting success.

A clear plan that aligns payment schedules and financing options with real cash flow makes acquisition risk manageable.

Summary: You can buy an existing business if you blend seller financing, government loans, selective equity, and creative structures so purchases match operational earnings.

Protect yourself with rigorous due diligence, a right‑sized purchase price, and a working capital reserve for early improvements.

Negotiate payment terms that flex by season and avoid debt or lease obligations the business cannot comfortably service.

Present clean documentation and a credible plan to strengthen credit and seller confidence, and keep lenders informed during the first years.

Move forward only when financing, payments, and integration align, then the acquisition can become a durable win for you and business owners.