Business Valuation for Exit Strategy

Business Valuation for Exit Strategy

Natalie Luneva

December 17, 2025

Business valuation for exit strategy is the disciplined process of determining what your company is worth today in the context of a future sale or transition. It goes beyond simple revenue multiples or “gut feel.” A valuation examines your financial performance, cash flow quality, customer contracts, operational maturity, and market conditions to produce a defensible market-based value range.

This isn’t a backend task for the final year of ownership; it’s foundational to shaping the entire exit trajectory. Formal valuations inform what buyers will support, what objectives are achievable, and what gaps you need to close years before a sale. Without that objective baseline, owners often misprice opportunities, concede value in negotiations, or rush into suboptimal deals under pressure.

Only about 20–30% of businesses that go to market actually complete a sale, in large part because most owners bring their companies to market unprepared and without a valuation-driven plan.

A robust valuation gives you clarity on realistic value drivers, highlights where to focus improvement efforts, and aligns your personal financial goals with what the market will actually pay. In what follows, we’ll break down the valuation process, the factors buyers care about, and how to use valuation as the engine of a strategic business exit planning.

A defensible market number should guide your plan, not the other way around. Starting with an objective assessment grounds expectations in today’s conditions and keeps your choices realistic.

A formal valuation shows what buyers will support now. That prevents you from chasing unrealistic goals and helps you set timelines that matter.

You can translate desired proceeds into clear milestones. Match your personal goals to achievable results so investments and decisions track toward a measurable target.

Three gaps appear: the Wealth Gap between personal net worth and required capital; the Value Gap versus top peers; and the Profit Gap in margins. Quantifying these gaps turns hope into tasks you can fix over several years.

Starting five to ten years in advance exposes diligence issues and tax or legal steps you can take in time. Early work on earnings quality, customer mix, and owner independence reduces the chance of rushed decisions if health problems or unsolicited offers arrive.

Use periodic valuation updates to measure progress and pick the best window to sell.

When a prospective acquirer reviews your company, steady cash and solid systems lead the list. Buyers scan four areas first: earnings, customers, leadership, and market position. You should make each one easy to verify with crisp evidence.

Show recurring revenue and clean, auditable profits. Normalize financials, document one-off items, and present trailing cash performance so buyers see sustainability.

Reduce single-customer risk and add contracts, multi-year renewals, and diversified segments. Buyers pay more when relationships are documented and retention is high.

Elevate management, delegate critical tasks, and codify processes. When owners are not the only decision makers, perceived risk drops and terms improve.

Articulate differentiation, pricing power, and a realistic pipeline. Buyers reward clear growth plans backed by capacity and capital needs.

Small changes in margins or a single large contract can shift how buyers price your company overnight. Focus on the levers that move multiples and act on the highest-impact items first.

Buyers look at historical revenue, margin trends, cash flow, and debt levels. Clean, GAAP-aligned statements and margin expansion plans raise price expectations.

Prudent debt management protects free cash flow and keeps financing options open during a sale process.

Cycles and capital markets shape what investors will pay. When funding is plentiful, multiples rise; when tight, underwriters get conservative.

Strong teams that can run without the owners reduce perceived risk. Documented roles and a clear succession plan directly lift perceived quality.

Recurring contracts, high retention, and durable differentiation make cash flow more predictable. That predictability earns higher multiples and shortens time to close.

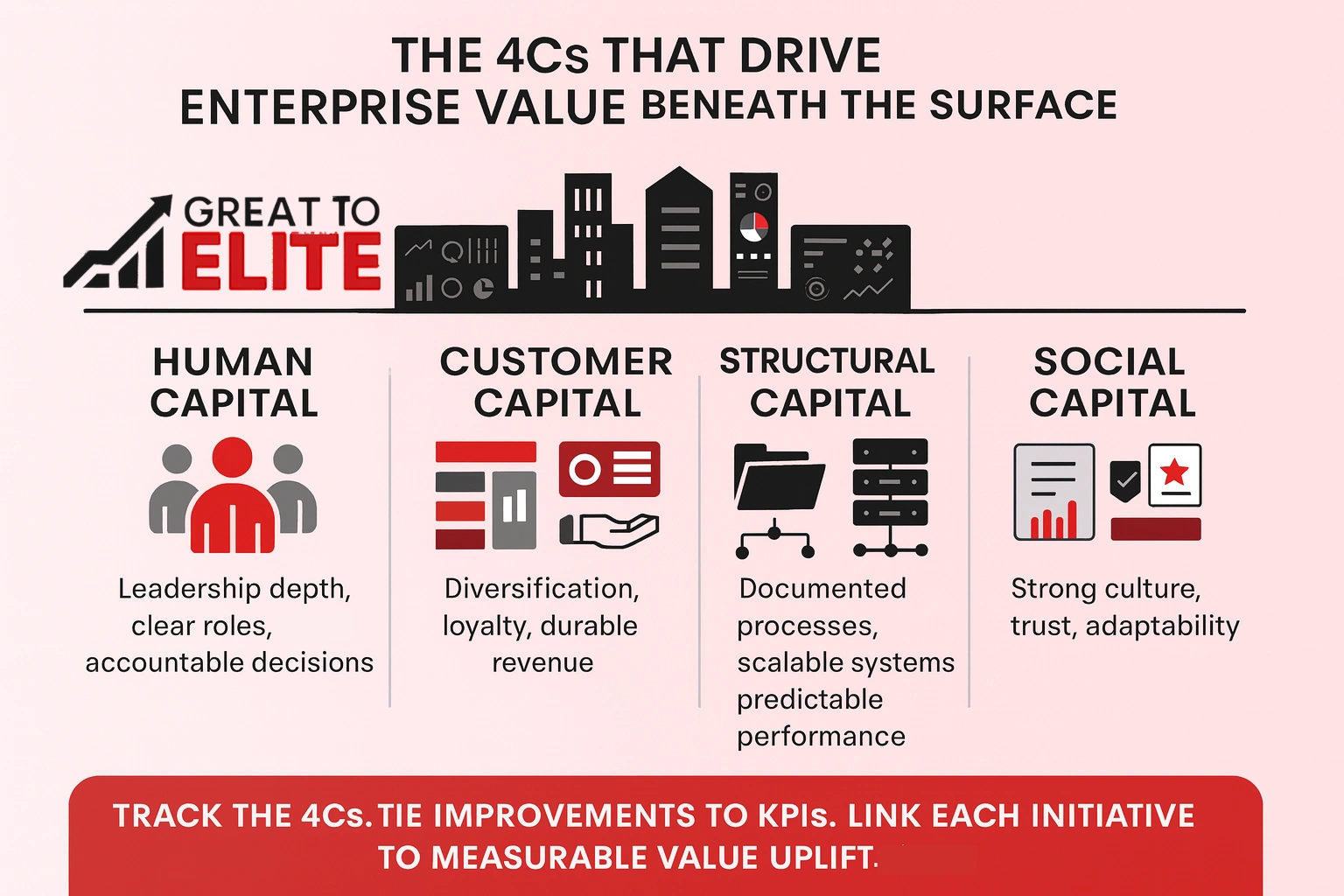

What sits beneath financial sheets, leadership, customers, systems, and culture, shapes long-term value. These four capitals reduce risk and make your company more sellable. Tackle them early so improvements are visible to buyers and advisors.

Deepen the leadership bench and clarify roles. Institutionalize decision rights so owners can step back without disruption.

Cut concentration risk, expand into nearby segments, and lock revenue with multi-year agreements. Link retention and lifetime value to pricing power.

Document processes, create SOPs, and automate workflows. Systems that scale make performance repeatable and simpler to forecast.

Codify values and behaviors that support trust and retention. A resilient culture speeds adoption of new systems and preserves performance during transitions.

Valuation approaches differ in focus: expected returns, market comparables, or tangible asset coverage. Each method answers a different buyer question and suits different data quality and lifecycle stages.

Income-based methods project future cash flow and discount it to present value using a risk-adjusted rate. Terminal value often drives most of the DCF result, so assumptions about long-term growth and discount rates matter.

Market-based approaches use comparable transactions and industry multiples to form a practical range tied to how buyers actually pay. This method reflects current market sentiment and investor return requirements.

Asset-based techniques set a floor, as they sum the fair market values of tangible and intangible assets and subtract liabilities. Use this when earnings are volatile or during liquidation scenarios.

Sector multiples vary. For example, illustrative ranges show healthcare facilities near 8.75x EBITDA, general retail about 16.63x, and REITs around 21.02x. These differences highlight how growth and risk shape buyer pricing.

A clear, repeatable process turns scattered numbers into an actionable price range you can trust. Assemble clean statements, schedules, and key metrics for the last three to five years.

Normalize owner-related costs, one-time items, and non-operating receipts so earnings reflect true operating cash flow. Reconcile income, balance sheet, and cash statements and produce tidy schedules that investors and buyers can test quickly.

Map demand drivers, sector conditions, and capital availability. Identify material risks that could depress offers and document likelihood and mitigation steps. That context shapes the multiple range you will use.

Benchmark against private and public peers. Choose multiples that match scale, margin profile, and growth. Harmonize outputs from different methods to form a defensible range.

Value contracts, IP, brand equity, and internal systems so nothing material is missed. Combine asset-based checks with income and market approaches to capture hidden upside.

Turn analysis into decisions: sequence initiatives, document working-capital flow, and add an example checklist for legal, tax, and operations readiness. Use the results to guide planning and timing so your company can capture the best terms.

Timing and structure start with an honest assessment of what your company can realistically deliver over the next few years. That clarity guides whether you pursue a full sale, an internal transfer, or a recapitalization.

You use the assessment to set realistic timing and deal shape. If a projected value supports cash at close, you may push for a clean sale. If not, earnouts or rollover equity can bridge the gap and share future upside.

A third-party sale often yields the widest price discovery. An internal transfer keeps continuity and rewards managers. A recap gives partial liquidity while preserving growth potential.

Start early so systems, contracts, and margin gains look credible by sale time. A three-year retirement target requires different steps than a ten-year plan.

Test base and stretch scenarios, surface sensitive items early, and measure progress annually. These steps make your plan actionable and improve the odds of cleaner deals and better terms when the time comes.

Timing can make the difference between a quick sale at a strong price and a drawn-out process that chips away at value. Read market signals and be ready to act when conditions lift multiples. Poor timing can force concessions and slow sales.

Macro cycles, sector health, and capital flows move multiples up or down. Track buyer interest, financing appetite, and customer cohorts so you can accelerate or pause outreach.

Focus on team independence, pursue credible new opportunities, and keep data clean. These lifts boost profit visibility and reduce retrade risk with buyers and investors.

A staged program prevents surprises and lifts bargaining power when offers arrive. Great to Elite turns scattered priorities into a clear, market-aligned plan you can execute without disrupting day-to-day operations.

Owners benefit from structured, phased engagements that deliver value step by step. Regular updates reduce risk and surface opportunities early.

Book a call to assess your starting point, align on goals, and map a 90-day plan that accelerates value creation.

A clear, market-rooted assessment turns vague hopes into concrete steps you can act on. Let a defensible number guide your exit planning so your expectations match what buyers will support today.

Commit to starting years in advance. Close gaps, strengthen operations, and prioritize the few initiatives that most lift worth and return. Combine methods thoughtfully, run a disciplined process, and refresh your business valuation regularly as conditions change.

Align personal goals with timing and tax outcomes, stay flexible on when to market the company, and pick advisors who keep your time focused on running things well. With a valuation-first plan you control the future and improve the odds of a clean, higher-value sale.