Family Business Succession Planning Strategies

Family Business Succession Planning Strategies

Natalie Luneva

November 9, 2025

Family Business Succession Planning is the process of preparing for the smooth transfer of ownership and leadership from one generation to the next. It involves defining who will lead the company, how ownership and decision-making rights are shared, and setting timelines, governance, and development steps to ensure the business continues successfully while protecting family relationships and the founder’s legacy.

It’s not a one-time event but a multi-year strategy that includes mentoring successors, clarifying roles, coordinating legal and tax considerations, and creating contingency plans for unexpected events.

Fewer than one-third of family-owned companies survive to the second generation, and only about 10-15% reach a third generation. That stark fact shows why leaving transitions to chance is costly.

Successful handovers take years of steady work, not a single decision at the end. Farm the company at home as one of several career options. This reduces pressure on your children and helps the next generation consider the role by choice.

Remember the odds: fewer than one-third of small family firms survive to the second generation, and roughly 13% reach a third. Those numbers show why early action matters. Treat this as an ongoing process that you revisit over time.

Encourage outside experience for three to five years so future leaders return with new skills and perspective. Give small, real responsibilities at work and model the leadership behaviors you want repeated.

Over months and years, these steps help align families and businesses on a realistic way forward. When you’re ready, Great to Elite can support the next phase of your plan.

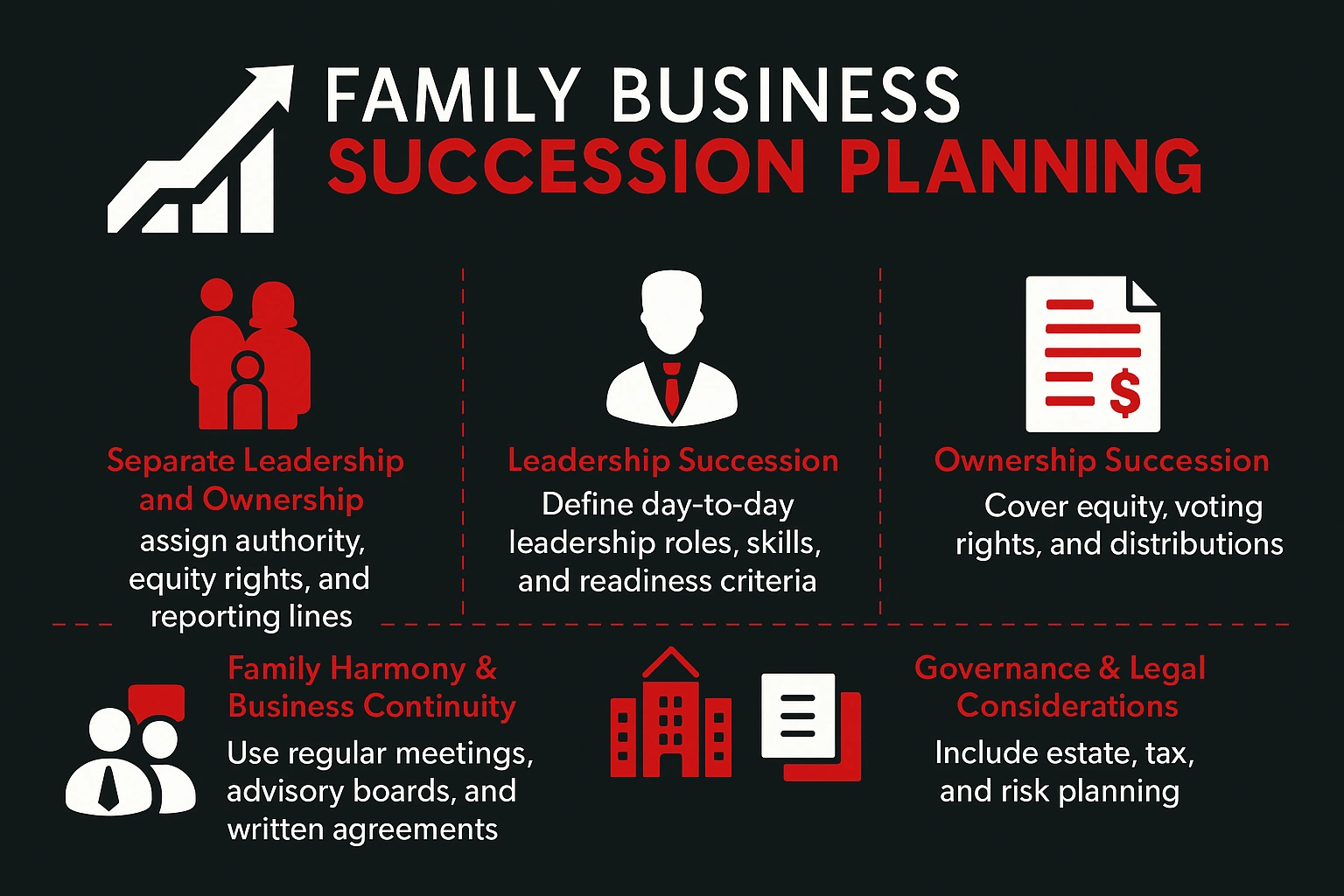

Clear structure prevents common conflicts. Separate operational leadership from ownership decisions. This helps you assign authority, equity rights, and reporting lines without mixing roles.

Leadership covers who runs day-to-day operations and sets strategy. Ownership covers equity, voting rights, and distributions. Make both tracks explicit in your written plan so expectations match legal documents.

Map roles for leaders, successors, and key family members. Define skills and readiness criteria for any successor so selection is fair and data-driven. Also set compensation and governance rules that apply equally to relatives and non-relatives.

Formal forums reduce tension. Use regular meetings and an advisory board to surface concerns and test decisions objectively. Capture agreements in writing to protect continuity when disagreements arise.

Documenting these elements creates a practical succession plan that protects legacy and keeps operations steady through the transition to the next generation.

Begin with a clear, evidence-based assessment to know exactly where the company stands today. Run a structured review of financials, operations, culture, and a SWOT so your next moves rest on facts, not assumptions.

Translate your vision into measurable goals and timelines. Use milestones that show progress at 6, 12, and 24 months so every stakeholder sees what success looks like.

Identify potential successors early. Map the skills each role needs and create tailored development paths, mentoring, role rotations, and external hires, to close gaps before the handover.

Draft the transition plan alongside your business and estate plans. Cash flow, tax impacts, and control rules interact; writing them together avoids surprises and preserves value.

Build an emergency succession plan that names interim authority and critical contacts to keep operations steady if an unexpected event occurs.

Select leaders by skills and track record, not by birth order or tradition. Start with clear, objective criteria for the successor role. Use measurable benchmarks so each candidate is assessed fairly.

Do not rely on birth order or gender to decide who leads. Define competency criteria and score applicants against them.

Encourage three to five years of outside experience. Returning candidates bring credibility and new ideas that improve the company.

Bring next-generation members into specific roles with deliverables and reporting lines. This clarifies expectations for employees and peers.

Pair potential successors with mentors who give candid feedback. Convene an advisory board with finance, legal, and industry expertise to guide development.

Map responsibility zones to prevent overlap and protect relationships. Hold successors to the same performance standards as other team members to build trust across the company.

A smooth handover rests on clear governance, reliable valuations, and coordinated tax strategy. Long before you set a handover date, align legal documents, estate guidance, and company tax strategy so timing, control, and cash flow do not collide.

Coordinate estate, tax, and risk strategies with your written plan to avoid surprises that can derail timing or voting control. Work with a lawyer and accountant to model tax outcomes and liquidity needs.

Commission periodic valuations so owners and leaders make informed decisions about buy‑sell terms, equity transfers, and financing continuity. Document contingency funding options to cover taxes, redemptions, or shortfalls.

Use formal pay structures tied to roles and performance to preserve fairness and retain key employees. Apply the same job descriptions and review cycles to relatives and non‑relatives to avoid perceived favoritism.

Hold regular meetings in neutral settings to surface hard topics and keep relationships strong. Convene an advisory board with legal, financial, and organizational expertise plus a seasoned industry voice for structured oversight.

A tailored, expert-led process aligns legal, tax, and leadership work so transitions run to schedule.

When you want a single partner to bring governance, valuation, and leader development together, Great to Elite delivers coordinated support. You get experienced advisors who know typical challenges and how to guide leaders toward clear outcomes.

Comprehensive support reduces risk and speeds readiness. That includes advisory board setup, facilitated meetings, and aligned emergency and long-range plans tied to valuation and liquidity.

Ready to secure your family business’s future with confidence? Contact Great to Elite today to start a succession plan tailored to your unique needs. Let’s build a clear, actionable path for leadership, governance, and growth together.

A durable transfer happens when you treat leadership change as a long game rather than a single event. Use a clear plan, set a handover date, and align legal and financial work so timing matches goals.

You improve the odds of success if you start early. Develop leaders methodically and align owners, the board, and company teams around milestones. This reduces avoidable challenges and keeps operations steady.

Protect your legacy and document agreements, communicate often, and empower the next generation with defined roles and standards. That clarity helps members step into the CEO role with confidence.

Engage advisors who coordinate governance, valuation, and leader development so the transition runs on schedule and your legacy endures.